新冠病毒疫情危机后供应商面临生存决策 | After COVID-19 Crisis, Suppliers Face Existential Decisions

进入2020年下半年,支撑起西方国家的航空航天和国防(A&D)工业基础的供应商开始面临生存危机。

Suppliers across the western aerospace and defense industrial base faced an existential crisis entering the second half of 2020.

商业航空旅行是民用航空工业的命脉,在2020年上半年,民用航空业受到了波音737MAX两次事故造成的打击,然后爆发了新冠疫情,这个产业又受到沉重一击。据金融分析师称,到2020年底航空公司的客运量可能只有2019年水平的55%左右。然而问题是到了2021年,如果仍然没有新冠病毒疫苗的出现,客流是否会出现显著增长。

Commercial air travel, the lifeblood of industry, took a body blow in the first half of the year with the one-two punch of the Boeing 737 MAX crisis and then the outbreak of COVID-19. Passenger air traffic could end 2020 at about 55% of 2019’s total level, according to financial analysts, and in 2021, the question will be whether a significant uptick can occur without a vaccine against the novel coronavirus.

对于制造商来说,他们预计飞机生产要等到2023-2025年才能恢复到2019年的水平。在这个十年的大部分时间里,数千架曾经在采购计划中的大型商用飞机将被取消,因为银行的援助的资金并不包括采购这些飞机的计划。有专家认为,航空航天和国防(A&D)领域的制造业产能过剩达30%~50%,并且20%的低级供应商可能受到经济威胁从而在未来几年退出该行业。回想一下在新冠疫性大流行之前,波音和空客这两家大型制造商的窄体机产能已接近那个疯狂的60年代,宽体机产能(已经很高)只是在相对几年内高增长预期的市场显的不足,而国防领域的预算预计将保持不变,仅需考虑市场上的通货膨胀情况。

In turn, manufacturers do not expect 2019 production levels to return until 2023-25, with thousands of once-planned large commercial aircraft now effectively erased from bankable plans for much of this decade. Experts see 30-50% excess capacity across aerospace and defense (A&D) manufacturing and a threat that around 20% of lower-tier suppliers could exit the industry in coming years. Recall that before the COVID-19 pandemic, monthly narrowbody production rates at the two leading OEMs were headed for the 60s, widebody rates were only softening against a predicted upswing in a few years, and defense budgets were expected to remain flat with only inflationary improvements.

Warbird Capital首席执行官兼首席投资官Nicholas Pastushan说:“对航空业来说,新冠疫情是小行星撞地球这样的潜在大规模灭绝事件。”

“COVID-19 is that asteroid hit that takes out the Sun,” says Warbird Capital CEO and Chief Investment Officer Nicholas Pastushan. “It looks like a potential mass extinction event as it comes to businesses in aviation.”

Pastushan在GE金融航空服务公司担任了六年的行业研究总监,随后在CIT运输业务中担任首席投资官超过十年。“我们过去将这样的事件描述为一场核战争,一场类似世界末日的事情‘我想我们无论如何都要死了,所以谁在乎呢?'嗯,实际上我们并没有死,但交通中断事件已经发生。”他说道。

Pastushan’s career includes six years at GE Capital Aviation Services, where he was director of industry research, followed by more than a decade as chief investment officer for the erstwhile CIT transportation portfolio. “We used to describe events like this as being, well, you know, a nuclear war, end-of-the-world kind of thing: ‘I guess we’re all dead anyway, so who cares?’ Well, we’re not dead, and this traffic disruption event has happened,” he reasons.

Pastushan和美国银行分析师Ronald Epstein都表示,他们预计市场对新型飞机的需求将直线下降。Epstein在6月的《航空周刊》网络研讨会上说:“如果2023年的确只是恢复到2019年的水平,那意味着在接下来的几年中,市场上不会实现增长,也不再需要新的飞机。传统上60%的新飞机交付将满足行业增长的需求,现在只有大约40%的飞机需要替换。”

Both Pastushan and Bank of America analyst Ronald Epstein say they expect demand for new-build aircraft to plummet. “If 2023 really is the year we’d get back to 2019 levels, that means for the next couple of years, no aircraft are needed for growth,” Epstein said during an Aviation Week webinar in June. “With 60% of new aircraft deliveries traditionally going to meet industry growth, now all that is needed is the roughly 40% for replacement.”

Pastushan说:“我们正在考虑有几年时间飞机产量为零的情况。”

“We’re looking at a couple of years’ worth of needing zero production,” Pastushan said.

Naveo常务董事Richard Brown在7月8日的报告中表示,2020年的新飞机生产可能有1090架,这只是2006年的水平。这相当于约710亿美元产值,比波音737MAX事故之前2018年的水平低了约500亿美元。

According to Naveo Managing Director Richard Brown in a July 8 report, 2020 new-aircraft production, likely around 1,090 airliners, will represent a return to 2006 levels. In production value, it will equate to roughly $71 billion worth of work—about $50 billion, off pre-MAX 2018 levels.

Frost&Sullivan顾问公司高级航空航天业分析师Timothy Kuder表示,到2025年,商用飞机制造业将损失4750亿美元,“我们认为这些产值本来都是来自飞机制造,但现在再也看不到了。”

Timothy Kuder, senior commercial aerospace industry analyst at advisor Frost & Sullivan, says the lost work through 2025 represents $475 billion in commercial aviation manufacturing, “which is just aircraft production we thought was going to be there but we’re never going to see again.”

Epstein和Pastushan都表示,预计飞机生产不会完全停止,因为完全停止的生产将为供应链和整个行业吹响丧钟。但是,随着飞机制造商寻求以最低可持续生产率进行生产,这对需要进行结构调整的行业来说将是不小的安慰。

Both Epstein and Pastushan said production is not expected to halt completely because that would be a death knell for the supply chain and industry altogether. But that will be little comfort to a wide swath of industry that faces the need to make structural changes as aircraft OEMs seek the lowest sustainable production rates of their products.

Avascent咨询公司负责民航业务的Jay Carmel表示:“整个供应链将要承受巨大的痛苦。”

“There is going to be tremendous pain throughout the supply chain,” echoes Jay Carmel, who leads the civil aerospace practice at advisor Avascent.

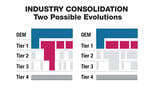

与其他许多行业一样,西方A&D制造业类似于金字塔的结构。排名靠前的有8~10个OEM和旗舰防务主承包商,以及大约十几个主要的一级供应商,这些一级供应商中有些企业的业务正逐渐与其OEM客户竞争。然后是几十个主要的二级供应商和一些较大的“小型”防务承包商,这是他们近十年来不断缩小规模的结果。三级供应商有15000个或更多的企业,其中许多供应商涉及多个行业,甚至包括消费品行业等。商用航空业务约占整个A&D行业的3/4,其余是防务领域的业务。

The Western A&D manufacturing sector, like many others, resembles a pyramid structure. The top counts 8-10 OEMs and flagship national defense prime contractors, and roughly a dozen major Tier 1 suppliers—with some of the latter increasingly rivaling their OEM customers in business activity. Then comes a few score of major Tier 2 providers and “big-small” defense contractors—a shrinking layer over the recent decade—and 15,000 or more Tier-3-plus suppliers, many of which feed into multiple industries but also include mom-and-pop shops. Commercial aviation business activity accounts for roughly three-quarters of the whole sector, and defense composes the rest.

如果从A&D金字塔向下看去,对行业下降的辐射担忧成比例增加。 Frost公司美洲地区A&D和安全部门副总裁Mike Blades说:“许多零件制造商都是小型公司,一家拥有多元化投资组合的大公司相比,这样的小型公司会遭受更大的打击,而多元化的大公司可以出售与航空业无关的业务或出售需求并没有下降的产品来渡过难关。我们将看到供应链会出现很多问题,甚至可能是公司倒闭。首要问题是供应链的状况并不理想。”

Fears of fallout increase proportionately as observers look further down the pyramid. “A lot of those small-part or spare-part manufacturers are smaller companies,” says Mike Blades, Frost vice president of A&D and security for the Americas. “They are going to be hit much harder by this than a larger company that has a diversified portfolio [and] can weather the storm by selling more of what they have on hand that is not aerospace-related or insulated from the decrease in demand. We are going to see issues in the supply chain and possibly companies going out of business. The supply chain was not in the best shape to begin with.”

的确,一些专家指出,下层供应商已经很容易陷入疫情的影响之中。“十年来,OEM迫使次级供应商投资提高生产率的工具,再加上波音的成功伙伴关系和空客的内部效率SCOPe / SCOPe +计划所不懈的进行成本削减,使航空航天供应链内部的资金匮乏,”Alton顾问在六月的报告中说。

Indeed, several experts note lower-tier providers already were strained going into the pandemic. “A decade of OEMs pressuring subtier manufacturers to make investments and tool up for production rate increases—coupled with relentless cost cutting through Boeing’s Partnership for Success and Airbus’ internal efficiency SCOPe/SCOPe+ programs—has left the aerospace supply chain capital-starved,” Alton advisors said in a June report.

第二季度,一些业内顶级首席执行官继续发出警报,尤其是关于他们的供应链。雷神技术公司首席执行官Gregory Hayes表示:“我真正的担忧是,尽管飞机用户将度过艰难的时刻,但此刻我最担心的是供应商中的小型企业。”

CEOs atop the industry continued to sound the alarm in the second quarter, particularly about their supply chain. “The real concern, if I think about everybody here, [is that] while the airline customers are going to have a tough time, it is the small business suppliers that I’m most worried about,” says Raytheon Technologies CEO Gregory Hayes.

空客公司首席执行官Guillaume Faury表示:“我们看到航空公司受到的打击严重,我们遭受的打击也很大,下一波打击将面向供应链企业。”

“We see the airlines are badly hit, and we are badly,” says Airbus CEO Guillaume Faury, “and the next wave is going to be the supply chain.”

哪些领域的企业风险更高?据多家公司预测,首先飞机结构制造企业处于最高风险区,因为此类企业的部门比较分散,而且其固定成本较高、税前利润率较低。客舱内饰也是会受到经济危机威胁的行业,此外MRO及零件供应商也不乐观,特别是对于当前的宽体机和可能要提前退役的老式客机。波音的供应链可能比空客的更加脆弱,因为波音737MAX已停产,而且除航空公司自己停飞的飞机以外,还有约800架库存的波音737飞机等待交付。

Who is more at risk? Many list aerostructures first, because the segment was fragmented and suffered higher fixed costs and lower pretax profit margins before the crisis. Interiors are another oft-cited sector under risk. Maintenance, repair and overhaul and parts suppliers also are listed, especially for widebodies and older airliners now likely to be headed for earlier retirement. Boeing and its suppliers are seen as more vulnerable than Airbus and its ecosystem, both because MAX production is practically null and because there are about 800 inventoried 737s to be delivered, in addition to customers’ own parked aircraft.

瑞银(UBS)的分析师在6月18日的报告中表示:“在我们恢复的基准假设下,2022年售后市场的销售额将达到2019年的65%~75%,而飞机OEM制造商的销售额到2024年将恢复到2018年的水平。”

“Under our baseline assumption of recovery, aftermarket sales will be 65-75% of 2019 in 2022, and OEM sales will be back to 2018 levels into 2024,” UBS analysts said in a June 18 report.

尽管如此,并不是每个航空领域的供应商都遭受了同样的痛苦,例如防务领域的供应商相对而言通常更安全。自疫情以来,五角大楼已向一些先进产品及其供应商进行了加速付款的流程,额度已达30亿美元,以使这些供应商的财务状况得到好转。

Still, not every vendor is suffering the same, and defense suppliers in general are relatively safer. The Pentagon has injected more than $3 billion in accelerated payments into primes and their suppliers to bolster their financial positions since COVID-19 hit the U.S. in force.

对此,防务领域的工业基础已经大大巩固,超出了政府官员在疫情流行之前担心的情况。相比之下,由于数十年来商业航空领域将大约2/3的项目支出外包给供应商,因此商用航空领域的工业基础仍然是很分散的。而且由于飞机有大量的、需要多年生产的积压订单,这使商用航空仍然有着上升的前景,这也引起了新的参与者和投资者更多的兴趣。

Moreover, the defense-industrial base already had consolidated substantially—to a degree that government officials were worried before the pandemic. The commercial supply base, by contrast, remains far more fragmented due to decades of OEMs outsourcing about two-thirds of their aircraft program spending to suppliers. Above all, the commercial segment faced rising prospects from a then-historic backlog of aircraft orders, driving more interest from new players and investors.

穆迪投资者服务公司(Moody's Investors Service)于6月表示:“过去十年来,国防承包商的低层供应商的合并为企业的弹性做出了贡献。与10年前相比,我们给美国国防承包商的平均评级是规模更大、运营更好,且更有活力。”

“Consolidation within the lower tier of defense contractors over the past decade has contributed to the sector’s resilience,” Moody’s Investors Service said in June. “The average U.S. defense contractor that we rate is simply a larger, better operated and more dynamic company than it was 10 years ago.”

根据穆迪的说法,“大多数”国防承包商由管理团队领导,这些团队经历并驾驭了《2011年预算控制法案》之后“具有挑战性的”七年,在所谓的超级委员会未能就削减联邦开支达到协议之后,该法案设定了项目预算支出上限。在随后的几年中,政府承包商的商业环境动荡不安,包括政府临时关闭、在最后关头艰难通过的两党预算交易,以及寻求低价交易且技术上可行的政府买家。

According to Moody’s, “most” of the defense contractors are led by management teams that experienced and navigated the “challenging” seven-year period following the Budget Control Act of 2011, the law that brought sequestration spending caps after a so-called super committee of lawmakers failed to find agreement on federal cuts. Subsequent years saw turbulent business conditions for government contractors, including government shutdowns and hard-fought, last-minute bipartisan budget deals, as well as government buyers seeking low-price, technically acceptable deals.

穆迪高级分析师Bruce Herskovics表示:“航空航天和国防领域企业的生产水平、计价服务时间、新业务开发等受到疫情爆发的影响很小。政府为保持设施开放和项目活跃所做的努力为这种稳定做出了贡献,这也反映了该行业的成熟。”

“Aerospace and defense companies’ production levels, billable service hours, new business development and collections have been only minimally disrupted by the COVID-19 outbreak,” said Bruce Herskovics, a Moody’s senior analyst. “Government efforts to keep facilities open and projects active have contributed to this stability, which also reflects the sector’s maturation.”

众多顾问认为,A&D供应商的工业基础已接近“过渡三阶段”中第一阶段的结尾,最初的严重危机开始减弱。在第一阶段,企业生存的可能性是通过资金流动性、可用于维持运营的现金和等价物等储备量来衡量的。罗兰·贝格(Roland Berger)公司全球A&D业务负责人Manfred Hader表示:“目前最大的担忧是如何确保这个行业在经济危机中实现平稳着陆。”

Numerous consultants suggest the A&D supplier base is nearing the end of the first phase of a three-step transition, and the initial deep crisis is beginning to wane. In the first phase, survival was likely as measured by liquidity, the cash and equivalents available to keep operating. “The biggest concern right now is how to ensure a smooth landing,” says Manfred Hader, who co-heads Roland Berger’s global A&D practice.

当供应商的经济状态转移到第二阶段(危机开始蔓延)时,企业必须准备承受长达24个月的“余震”,并准备多个“假设这会发生”的备用计划。“此时他们的计划应该包括类似‘壮士断腕’的举动(如产能合理化,即降低产能),以及随着特定情况的发展而计划触发更为激进的行动,甚至进行本来需要长远计划的重大战略举动(例如业务拆分剥离)。事先准备这些计划可以使公司一旦出现这些情况就可以迅速采取行动。”Alton报告说。他们建议公司设立专门的内部团队来进行这些计划的准备,而其他的经理们则专注于日常运营。

As the supply base shifts into the second phase—the pandemic overhang—companies have to prepare for up to 24 more months of aftershocks to the industrial base and have multiple “what-if” plans ready. “They should consist of no-regret moves (e.g., capacity rationalization), more aggressive actions triggered as specific scenarios unfold and big strategic moves (e.g., spin-offs) that need to be planned in advance so the company can move fast once it has a green light,” the Alton report said. Companies are advised to set up special internal teams dedicated to this side-planning, while other managers focus on daily operations.

毕马威(KPMG)的顾问在5月的报告中指出,在第二阶段,供应商将被迫采取积极行动来重塑业务,因为历史上对航空业造成重大冲击(例如9.11事件或2008年金融危机)的教训证明,企业不应该仅仅试图回避这些危机。他们表示,采取迅速果断行动的公司的表现比那些向危机“屈服”的公司要强3~4倍。

In this second phase, suppliers will be pressed to take aggressive action to reshape their businesses, according to presentations by KPMG consultants in May, as lessons from prior aviation shocks such as 9/11 or the 2008 financial crisis proved companies should not just try to ride it out. “Companies that took swift and decisive action outperformed those that ‘hunkered down’ by 3-4 times,” they said.

然而,现实的挑战更为复杂,因为上述建议只是笼统的一概而论,具体到每种情况并不一定都适用。例如,尽管宽体机目前的问题更大,但这并不意味着每种宽体机都处于同样的困境,而波音787的处境预计会更好。在窄体机中,更大的、航程更远的A320neo系列的表现有望至少在未来几年内优于波音737MAX。

Complicating the challenge, however, is parallel advice against making sweeping conclusions. While widebody aircraft are having issues, for instance, it does not mean every twin-aisle type is suffering equally; the Boeing 787 is expected to fare better. In narrowbodies, the larger, longer-range A320 family is expected to perform better than MAXs for at least a few years.

“在这种低迷时期,这种(区别不同情况的)处理方式是更为精确的方法,因为并不是每个人都会受到同样严重的影响。” Robinson and Cole的合作伙伴Jeff White说到。

“This is a much more surgical approach in this downturn,” Robinson and Cole Partner Jeff White says. “Not everyone will be impacted equally and hugely.”

同时,几位行业经理的外部顾问确信,A&D行业已进入一个拐点,类似于1970年代的石油危机、1990年代冷战结束,或9.11事件之后的行业转型。其中一个主要决定因素是,在行业反弹之前,其总的商业活动预计将从高峰下降约50%而到达低谷,最后阶段将与第二阶段同时开始,并有可能在进入到2021年之时转为增长趋势。

At the same time, several outside advisors to industry managers are certain A&D has entered an inflection point akin to transformations after the oil crisis of the 1970s, the end of the Cold War in the 1990s or after 9/11. A leading determination is that total business activity is expected to fall roughly 50% from peak to trough before a rebound takes root. This final phase will begin concurrently with the second phase of pandemic overhang and likely pick up momentum into 2021.

毕马威(KPMG)的顾问表示:“虽然原因并不重要,但我们的前提是行业已倾向于走向经济拐点,无论是向上还是向下。”

“Cause does not matter, but our premise is that industries tend to evolve at economic inflection points, both upturns and downturns,” KPMG consultants say.

在第三阶段,产业基础可能出现几种趋势从而重新被定义,如供应商整合、供应链区域化、政府对关键技术能力的投资进行重新分配、A&D的业务和服务的数字化、OEM从外包转向内包等。而业务弹性、区域化和成本降低将是主要的发展动机。

In this third and final phase, several trends will play out to redefine the industrial base: supplier consolidation, regionalization of supply chains, redomiciling and/or government investment in critical technology capacity, digitization of business practices and services across A&D, OEM insourcing and others. Resiliency, regionalization and cost reduction will be leading motivations.

因此,预计会有更多的并购以及所谓的非核心业务资产的剥离,并且私募股权投资人预计将在未来发挥尽可能重要的作用。同时,人们也看到政府在A&D行业中那些幸存下来的企业里将发挥更大的作用:由于政府提供了援助而获得股权从而成为直接利益相关者,未来政府也在确定企业优先事项方面具有更大的发言权。这些事件范围从要求发展“更环保”的客机,到决定相对于信托资本和反垄断当局来说谁是买家。

Thus, more mergers and acquisitions are expected as well as divestments of so-called noncore usiness assets, and private equity investors are expected to play as much of a role in the future as they have to date. At the same time, governments are seen playing a larger role in legacy industry affairs, too, from being direct stakeholders due to bailouts to having a larger say in setting priorities . These range from requiring “greener” airliners to deciding who can buy what vis-a-vis “trusted capital” and antitrust authorities.

此外,已经发生的一些行业举动将引发另外的问题。瑞银(UBS)分析师指出:“维持健康的供应链是一回事,但供应链关闭后再进行整顿又是另一项挑战。此外,有些供应链已经关闭;而在某些地方,供应链已经关闭、开启,然后又再次关闭;在其他一些地区,供应链则从来没有关闭过。这意味着以减产来应对需求不足的状况可能要持续到2021-2025年。

Furthermore, issues will emerge from actions that already have occurred. “Maintaining a healthy supply is one thing, but reforming the whole thing after turning it off is another challenge entirely,” UBS analysts note. “Moreover, not only has the supply chain been turned off, in some parts it has been turned off, turned on and then turned back [off] again. In some other areas, suppliers were never turned off, which means years of underproduction versus a new lower demand profile await them in 2021 to 2025.”

本文摘自Flight Paths Forward专题。在目前新冠疫情中航空业期望复苏阶段,本专题系列文章对航空产业的未来进行了深度的解读。点击这里获取更多信息。

Related Content