新冠疫情之后,随着制造业重新洗牌,规模将变得至关重要

如果你现在喜欢大型航空航天和国防公司的骨干企业,以后你会更爱他们。预计新型冠状病毒将在航空航天和国防(A&D)制造业中发挥催化作用,其中一个主要趋势是,大公司将通过吞并其他公司或收回更多工作而变得更庞大。

If you like the cadre of big aerospace and defense companies now, you are going to love them later. Among the major trends the novel coronavirus is expected to catalyze within aerospace and defense (A&D) manufacturing is that the big will get bigger by gobbling up others or taking back more work.

几位高管和顾问表示,未来几年,垂直整合的势头应该会有所回升。经过数十年的OEM,首要和顶级公司外包其项目的主要工作后,许多人看到趋势逆转,更多工作将回归内部。

In the next few years, vertical integration should pick up momentum, according to several executives and consultants. After decades of OEMs, primes and top-tier companies outsourcing major work on their programs, many see the pendulum swinging back to bringing more of it in-house.

一位顾问表示:“我们已经看到行业内出现了更多纵向一体化的迹象,随着我们在危机中做出的努力,其中一些整合可能会加速。”

“We’ve already seen signs of more vertical integration coming through the industry and potentially where some of that could be accelerated as we work through the crisis,” says one advisor.

几年前,波音将航空电子设备和其他细分市场分包出去,开始了这种趋势。随着雷神公司和联合技术公司以及L3技术公司和哈里斯公司的合并,重大合并再度兴起。现在,无论是保护利润还是确保供应,随着行业在新冠肺炎危机中重新洗牌,自主承担更多工作的理由正在快速增加。

Boeing started this a few years ago as it insourced avionics and other niche segments. Major consolidation picked up last year with the mergers of Raytheon and United Technologies Corp. and L3 Technologies and Harris Corp. Now, whether it be protecting profits or securing supply, the reasons to own more of the work are burgeoning as industry is refashioned in the COVID-19 crisis.

罗兰贝格的顾问Robert Thomson和Manfred Hader表示,首先,航空航天供应商面临着规模经济的缩减,但在生产中固定成本的比重更大,盈利能力和竞争力可能会下降。通过内部采购和获得额外的工作量,所谓的有机收入增长是可能的,但仅限于有限的程度。同样,由于设备和运营费用结构的原因,固定成本的降低仅在一定程度上是可行的。因此,合并是要考虑的重要杠杆。

For starters, aerospace suppliers are facing diminished economies of scale but a greater share of fixed-cost in production, with a likely loss in profitability and competitiveness, say Roland Berger advisors Robert Thomson and Manfred Hader. So-called organic top-line increases, through insourcing and acquisition of additional work packages, are possible but only to a limited degree. A fixed-cost reduction likewise is only feasible up to a certain level due to equipment and overhead structures. So consolidation is an important lever to consider.

部分原因在于2级及以下供应商陷入财务困境,出现了让他们抱团的机会。

Part and parcel to that will be the financial distress into which suppliers in Tier 2 and below fall—and the opportunity to roll them up.

顶尖公司的CEO们正在观望。5月13日,霍尼韦尔国际公司董事长、首席执行官兼总裁达Darius Adamczyk在一次投资者会议上发表讲话时提到了一个拐点。他对高盛(Goldman Sachs)表示:“几年来,我一直在谈论这是一个卖方市场,而不是买方市场。“但这种算法可能在今年下半年发生变化,我认为它可能会变得更像一个买方市场,估值可能会更好,也可能有所不同。这是我们想参与的。”

Top CEOs are watching. Speaking May 13 to an investor conference, Honeywell International Chairman, CEO and President Darius Adamczyk cited an inflection point. “For a couple of years now, I’ve been talking about how it is a seller’s market, not a buyer’s market,” he told Goldman Sachs. “But that calculus may change in the second half of the year, and I think it could become a bit more of a buyer’s market, and the valuations may be better and different. That’s something that we want to partake in.”

助长这种现象可能是出于可靠性和地缘政治原因,希望让供应更接近国内。海外供应商一度因其低成本而备受推崇,但突然间,他们被视为易受流行病、经济压力和全球贸易战影响的群体。反过来,咨询公司希望行业领袖们重新审视对当地有利的一面。

Feeding the phenomenon could be a desire to bring supply closer to home, both for reliability and geopolitical reasons. Suppliers overseas once were revered for their low-cost footprint, but suddenly they are seen as vulnerable to pandemics, economic stress and global trade wars. In turn, consultants expect industry leaders to take another look at favoring local regions.

即使是在目前被认为在经济衰退期间更安全的国防领域,也有人说大公司会变得更加强大。Capital Alpha Partners董事总经理Byron Callan在5月13日指出:“业内大公司应该会安然度过这场大流行,但可能着眼于较低的支出增长期望值。”“因此,并购在实现增长方面可能更为重要,尽管2021-2025年不会是有机增长。”

Even in the defense realm, which for now is considered safer during this downturn, there is talk of larger firms becoming even more powerful. “Large pure-plays should come through the pandemic relatively unscathed but may be looking at lower spending growth outlooks,” Capital Alpha Partners Managing Director Byron Callan noted May 13. “Mergers and acquisitions may thus be more important in delivering growth—even though it’s not organic growth—in 2021-25.”

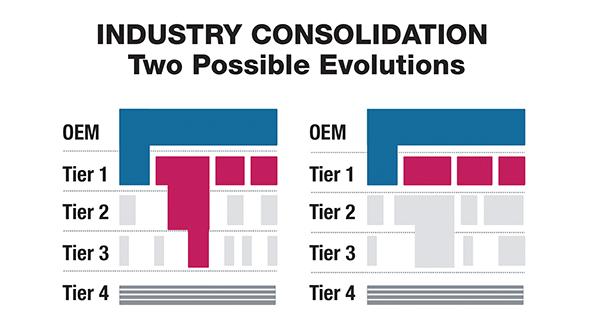

那么在哪里可以找到垂直整合与合并契机呢?根据顾问的报告,线索已经浮现。首先,看看主要供应商已经普遍涉及的环境和飞行控制系统、起落架、电力和内饰以及其他尚未涉足的领域,包括维护、维修和大修、物流、飞机结构和发动机。

So where to look for vertical integration and consolidation from the top? Clues are already emerging, according to advisor presentations. First, look at niches where top suppliers already are prevalent—environmental and flight-control systems, landing gear, electrical power and interiors—and others where they are not there yet, including maintenance, repair and overhaul, logistics, aerostructures and engines.

接下来,从顶级供应商的角度来看供应基础。谁会受到伤害并降低信贷额度?某些潜在目标的收入组合是什么?例如,商业与国防、产品与服务、老平台与下一代平台?

Next, look at the supply base from the perspective of a top supplier. Who is distressed or drawing down credit lines? What revenue mix do certain potential targets have—e.g., commercial vs. defense, products vs. services or aging vs. next-generation platforms?

最后,考虑新的整合核心将会在哪里。是否会出现更多的“超级1级”(如雷神公司),或者2级和3级供应商之间发生联合?据罗兰贝格(Roland Berger)称,前者可以使1级到3级的零件生产能力合理化,例如,超级1级可以通过价值链控制确保并防止次级供应商失败。后者可能是由机会驱动的,而不是遵循任何总体行业逻辑。

Finally, consider where the new nucleus of consolidation will be. Will more “super Tier 1s” such as Raytheon Technologies emerge, or will conglomeration occur among Tier 2 and 3 providers? The first would allow rationalization of capacity for detailed part production from Tier 1 to 3, for instance, with the super Tier 1s able to secure through-value-chain control and prevent subtier supplier failure, according to Roland Berger. The latter likely would be opportunistically driven rather than following any overarching industry logic.

正如一位顾问所说,对于规模较小的供应商来说,这些问题更加简单。你是想做一个买家,一个卖家还是想冒这个险?当然,这是一个较为简单的问题,但也同样难以回答。

For smaller suppliers, the questions are more concise, as one consultant says. Do you want to be a buyer, a seller or risk it as is? A simpler question, for sure, but no less difficult to answer.

这条消息是Michael Bruno在 Aviation Week & Space Technology 发表的文章。《Aviation Week & Space Technology》由人脉最广、经验最丰富的记者团队提供支持,为新趋势、最佳操作实践和政策、要求和预算的持续更新提供关键情报。 点击此处查看有关 Aviation Week & Space Technology 更多消息。