All current indicators point to continued strong cargo-conversion work, according to IBA Cargo Analyst Jonathan McDonald. These include number of conversions, shops and MROs active, and aircraft types offered for conversion.

E-commerce demand remains strong, as does Asian cargo demand. However, McDonald’s colleague, IBA Chief Economist Stuart Hatcher, cautions that inflation and interest rates are signaling a possible recession, which could cause temporary slack in demand for freighters.

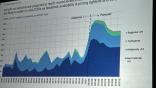

In a recent webinar, McDonald noted that freight rates rose as much as 27% in the year to March 2022, and most do not expect these rates to return to pre-pandemic levels until 2024-25.

High rates are reflected in cargo conversions. The fleet of converted Boeing 737-800s doubled in the past year, and “every day there is another one,” McDonald says. 757-200s and 767 conversions have stabilized as these programs have become mature.

Conversions of Airbus A321s, 330-200s and 330-300s are still small in number, but increasing fast.

The big news remains, in McDonald’s view, “the extraordinary upsurge in -800 conversions.” He calls 737-700 conversions “nichey,” as the -800 offers more pallets. Similarly, the A321 offers “more pallets per buck” than the A320.

In addition, the increasing number of conversion centers, MROs and locations active in converting A320-200s indicates emerging demand. Only 16 have been converted so far, but “there will be a lot more,” predicts McDonald.

Conversion centers for A330s are also expanding beyond the original EFW shop in Dresden, which alone expects to offer 60 slots for A330 conversions in a couple of years.

McDonald is impressed by IAI’s and Ethiopian’s new conversion shop for 767-300s in Addis Ababa. “Ethiopian is well known for high quality, and it is thrilling to see a conversion center in Addis,” he says.

According to McDonald, 777 conversion shops are also increasing, with NIAR WERX and Mammoth Freighters “also in the game,” in addition to IAI.

McDonald calls Embraer’s proposed E190 and E195 cargo conversions a “bold move,” but expects volumes will be limited. “It’s between ATRs and Q400s and smaller jets. I don’t think there is a huge space for that aircraft, and it could be expensive to convert.”

The Russia-Ukraine war should not have substantial impact on cargo markets, with only 23 cargo aircraft leased to Russian carriers. But detouring around Russia will add costs and require more capacity from the market, as will grounding of the small Russian fleet.

McDonald observes that values and lease rates for freighters have been considerably less volatile than for passenger aircraft in the past two years. The proposed new A350 and 777-8 freighters should sell for well over $150 million, with the 777-8 more valuable due to nine more tons of capacity.

Freighter fleets will be slower in reducing emissions than passenger fleets—an increasingly important consideration because converted freighters are generally older and less fuel-efficient. However, McDonald says “the A350 and 777-8 will be cleaner.”

The big takeaways on conversions, says McDonald, are that “-800s are doubling, Boeing is still dominant, but Airbus is gaining traction.”

Pressed by questioners on whether there could be an oversupply of freighters or a slackening of cargo demand, McDonald acknowledged there is always a risk of overcapacity. He cited strong e-commerce demand and increasing cargo demand through Anchorage, Seoul, Hong Kong and Singapore and within China as buttressing the market.

Still, IBA’s Hatcher noted that “inflation is up massively, oil prices are up [and] interest rates are rising. We could be on the precipice of recession.”

Presumably, that would mean only a hiccup in cargo growth and short-term uncertainty. But it’s a risk, like pretty much every aspect of aviation markets these days.

Related Content