Airbus’ Move To Reintegrate, Centralize May Have Far-Reaching Effects | エアバス社の再統合と集中化の動きが、広範囲に影響を及ぼす可能性

エアバス社は4月中旬、経営陣の大規模な変更を正式に発表した。Airbus Defense and Space社CEOのDirk Hoke氏は、カリスマ的な人気を誇ったCTO・Grazia Vittadini氏に続き、今夏のうちに退任する。さらに、影響力のあるCOOのポジションには Alberto Gutierrez氏が就任し、現COOのMichael Schoellhorn氏はHoke氏の後任となる。そしてこの発表から2週間後、エアバス社CEOのGuillaume Faury氏は機体製造基盤のさらなる統合を促進するための事業再編を発表した。

表面的には、今回の人事異動と事業再編にはあまり共通点がないように見える。しかし、Faury氏がエアバス社CEOに就任してから2年が経過した今、あるテーマがより明確に浮かび上がっている。それは集中化と統合化の強化で、Faury氏に特に忠実な幹部により管理されてきた。Hoke氏は長い間CEO就任の野望を秘めていたが、取締役会がFaury氏を選んだことで、その希望は打ち砕かれた。Vittadini氏もまたFaury氏の側近とはいえず、エアバス社エンジニアリング部門のトップであり、Faury氏と親密なJean-Brice Dumont氏と対立することもあった。これまでエアバス社の上級幹部ではなかったGutierrez氏の起用は、舞台裏では引き続き社内政治と戦術が重要な役割を果たしていることを示している。

最新の動きは、エアバス社の複雑な事業構造の一部に関わるものだ。 Faury氏は機体製造事業の大部分を再びエアバス社のコアビジネスとして取り込む計画を進めているが、同時に細かな部品製造を担う会社について、後日売却が可能な会社の洗い出しも進めている。なお、この計画は4月21日に詳細が説明された労働組合との交渉を前提としているため、計画の細部は変更される可能性がある。しかし、この決断そのものには疑問の余地はない。

経営陣は、機体製造子会社のPremium Aerotec社とStelia Aerospace社が担う業務のほとんどは、エアバス社とその将来の根幹をなすものであり、売却すべきではないと結論づけている。Faury氏は、エアバス社がデジタル設計・製造・サービス(DDMS)戦略に移行し、この3つのフェーズをデジタルで統合することで、設計および製造プロセスのより広範な部分を厳密に管理する必要があると主張している。それは、Spirit AeroSystems社が製造する737の胴体のような、ボーイング社がサプライヤーからの調達を選択するような大型部品も例外ではない。DDMSは、将来エアバス社が開発する全ての新型機の基盤になるものだ。同社は、2035年に就航予定の水素エンジン搭載機よりも前に新規プログラムを立ち上げることはないとみられているが、DDMSはA322(A321neoの機体延長・主翼変更・エンジン変更版)やA350貨物機といった(現時点では構想段階の)派生型の製造に使用される予定だ。

2022年初頭に開始される予定の再編計画は、フランスにAerolia社、ドイツにPremium Aerotec社を設立した2009年の決定から逆行するものだ。Aerolia社は後に別の子会社であるSogerma社と合併し、Stelia Aerospace社となった。エアバス社としては、前CEOの Tom Enders氏が率いた経営陣の下、ボーイング社がSpirit AeroSystemsを売却したように、Aerolia・Premium Aerotec両社を売却することを目論んでいた。しかし実際には、リーマン・ショック後の需要低迷によりそれは起こらなかった。

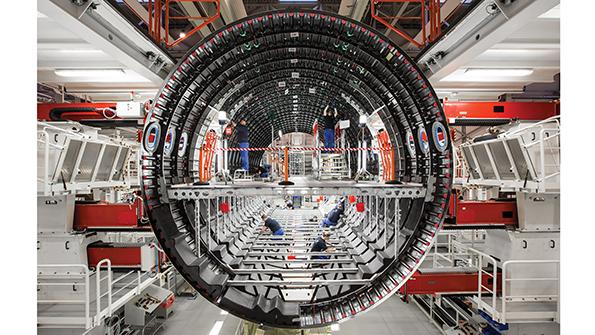

Premium Aerotec社はドイツのアウグスブルクに本社を置き、ファーレルとノルデンハムにも工場を持っている。Stelia Aerospace社はフランスのメオルトとサン=ナゼールにある機体工場で構成される。両社とも各種エアバス機の胴体セクションまでのサブアッセンブリーの製造を担っている。

今回の計画では、3つの新会社が設立される予定だ。1社はフランスを拠点とし、現在のStelia社の事業とエアバス社のサン=ナゼールおよびナント工場の事業を統合する。この新会社では、全エアバス機の胴体先端部および翼胴結合部、A320の前部胴体、A330およびA350の中央胴体などの製造を受け持ち、16の拠点で12,000人の従業員を抱えることになる。

もう1社はドイツに設立され、この新会社はドイツにある全てのPremium Aerotec社の施設(アウグスブルクの第4工場とファーレルの同社施設を除く)と、エアバス社のスタード拠点およびハンブルクの組み立て工場を統合する。ここではA330およびA350の前部胴体、A320の中央胴体、全エアバス機の後部胴体およびテイルコーンが製造され、5ヶ所の拠点で7,000人の従業員が雇用される予定だ。

この2社は、もはやエアバス社のサプライヤーとはみなされず、エアバス社の生産システムやフローに統合されるが、それでも独立した別個の企業であり続ける。

3つ目の新会社は各種部品に特化し、年間売上高9億ユーロ(約11億ドル)を見込んでいる。この新会社はファーレルにあるPremium Aerotec社の拠点、アウグスブルクの同社第4工場、そしてルーマニアのブラジョヴにある施設を統合する。なお、エアバス社は部品事業について「最適解を見きわめるため、様々な所有形態を検討している」としている。同社としては「適切な投資戦略」により、複雑化する部品業界において、持続可能で競争力を持つ強力なグローバル企業を生み出すことができると考えている。この新会社はエアバス社を主要顧客とすることで「長期的な成長視点」を得られるが、民間向け/防衛向け製品について外部顧客とのビジネスを行うこともあり得るとしている。

この会社では、機械加工・フライス加工・旋削加工による金属および非金属部品の 製造を行うことになる。

今回の再編は、エアバス社がサプライヤーに任せる業務の境界線を明確にし、細かな部品の自社製造は必須ではないと考えていることを示している。一方で、各地に分散している拠点の整理が必要かどうかについては言及していない。少なくとも短期的には変化する予定はないが(というより不可能だろう)、将来的には疑問が残る。ドイツのブレーメンにあるエアバス工場の役割については社内で議論が続けられてきたが、Faury氏はまだ結論を出していない。また、EUを離脱したイギリスに所在する拠点についてもどこかの時点で対応する必要があるが、大きな変更がされるのは新型機開発プログラムのワークシェアを決めるタイミングになるだろう。

ヨーロッパ全域の拠点を整理するという、考えにくい未来予想よりも重要なことは、今回の再編による副作用、つまりエアバス社本体の機体製造能力の強化だ。エアバス社が自社でまかなえる作業が増えることは、サプライヤーにとっては脅威となる。業界関係者によると、そう遠くない将来に直接的な影響を受ける可能性があったり、この動きが将来的に何を意味するか心配し始めている一部のサプライヤーには、エアバス社からのメッセージがすでに届いているという。

その中でも特に不安を増しているであろう2つの会社が、Spirit AeroSystems社とLeonard社だ。Spirit社は複合材製のA350中央胴体とA220の翼部などを、Leonard社はA220の水平および垂直尾翼を製造している。エアバス社はA220のサプライヤーと契約条件の再交渉をしようとしていた時に新型コロナウィルスのパンデミックが発生し、減産を余儀なくされたが、同社としては前メーカーであるボンバルディア社には実現できない好条件を目指していた。同様にA350もコスト削減のプレッシャーにさらされており、月産10機から5機以下まで落ち込んだことで、状況はさらに悪化している。

複数の業界関係者によると、エアバス社はA220だけでなくA350についても、主要サプライヤーと新たな契約を結ぶことを明らかにしたという。同時に、エアバス社はA350の生産技術向上のためにアウグスブルクおよびノルデンハムの工場に巨額の投資をしてきたが、現在そのインフラは有効活用できていない。

なお、短期的にはスペインのカディスにある拠点が注目されており、そこにGutierrez氏の起用が関係している。カディスのプエルトレアル工場の再建計画は、A380プログラムの中止や他のワイドボディ機の低迷により大きな打撃を受け、約300人の雇用が脅かされている。同社は「社会的パートナーと協力して、事業構造を最適化するための解決策を探っていく」としている。エアバス社のビジネスにおけるスペインの存在感は、常にフランスやドイツの影に隠れてしまっていることから、たとえカディスのような小規模拠点であっても、どのような動きを取ったところで大きな政治的反発を招くことは確実だ。

反発に直面する可能性について、Faury氏は常に気に留めておく必要がある。エアバス社がサプライチェーンの領域を取り込む形でさらに拡大し、集権化していくことは、不測の事態が起きた際のリスクも増大させることになる。会社にとってはプロセスの厳格な管理が求められ、Faury氏もここで勝負に出たからには、結果を出す必要があるということだ。

Aviation Week Intelligence Network (AWIN) のメンバーシップにご登録いただくと、開発プログラムやフリートの情報、会社や連絡先データベースへのアクセスが可能になり、新たなビジネスの発見やマーケット動向を把握することができます。貴社向けにカスタマイズされた製品デモをリクエスト。

Airbus formalized some pretty significant changes to its senior leadership in mid-April: Dirk Hoke, the CEO of Airbus Defense and Space, confirmed his departure later this summer, as did Grazia Vittadini, the charismatic and popular chief technology officer. In addition, the influential chief operating officer (COO) position will soon be held by Alberto Gutierrez, while incumbent COO Michael Schoellhorn will replace Hoke. Two weeks later, CEO Guillaume Faury announced more changes, this time to the industrial setup, fostering deeper integration of aerostructures manufacturing.

On the surface, the staff moves and industrial reorganization may not appear to have much in common. But a theme is emerging more clearly of late, two years after Faury moved into the Airbus CEO role: Centralization and integration are being reinforced and will be managed by a team of executives particularly loyal to Faury. Hoke has long had ambitions to become CEO, hopes that were dashed when the board opted for Faury. Vittadini, who has also not been part of Faury’s inner circle, sometimes clashed with Jean-Brice Dumont, Airbus head of engineering and a close associate of Faury. The appointment of Gutierrez, who has so far not been in the top tier of Airbus executives, shows that politics and tactics continue to play a role behind the scenes.

The latest action concerns a part of Airbus’ complex industrial setup. Faury is proceeding with his plans to reintegrate a large part of the aerostructures work into the core Airbus business while also carving out a detailed parts company that could be sold later. The plans are subject to negotiations with unions, which were briefed in more detail on April 21, which means there could still be changes to the setup—though the decision itself is not in doubt.

Management concluded that most of what aerostructures subsidiaries Premium Aerotec and Stelia Aerospace do is so core to Airbus and its future that they should not be sold. Faury argues that Airbus’ move into the digital design, manufacturing and services (DDMS) strategy, which integrates the three phases digitally, makes it necessary to keep tight control over a broader part of the design and manufacturing process—even of larger components that Boeing is happy to source from suppliers, such as 737 fuselages produced by Spirit AeroSystems. DDMS is the basis upon which Airbus plans to develop all future generations of aircraft. And while Airbus is unlikely to launch any new programs before its planned move into the next generation of hydrogen-powered aircraft slated for entry into service by 2035, DDMS will be used to build derivative aircraft such as a possible A322 (a stretched, rewinged and reengined version of the A321neo) or a freighter version of the A350.

The move, to be implemented at the beginning of 2022, would reverse an earlier 2009 decision to set up two aerostructures companies in France and Germany, Aerolia and Premium Aerotec. Aerolia later merged with Sogerma, another subsidiary, and was renamed Stelia Aerospace. Under the previous management team led by former CEO Tom Enders, Airbus had hoped to sell both Aerolia and Premium Aerotec—much like Boeing sold Spirit AeroSystems. But the sales never happened, in part because demand dropped in the aftermath of the global financial crisis.

Premium Aerotec is based in Augsburg, Germany, and has additional factories in Varel and Nordenham. Stelia Aerospace mainly comprises aerostructures facilities in Meaulte and Saint-Nazaire in France. Both companies build subassemblies up to fuselage sections across the range of Airbus products and divisions.

The latest plans call for the creation of three new companies. One would be based in France and combine the current Stelia businesses with Airbus sites in Saint-Nazaire and Nantes, France. That entity would produce, among other things, the nose fuselage and center wingboxes for all Airbus programs, the forward fuselage of the A320 and the central fuselage of the A330 and A350. It would have 12,000 employees at 16 sites.

Another new company is to be created in Germany. It would bring together all German Premium Aerotec facilities—except Augsburg’s Plant 4 and the company’s facilities in Varel—with Airbus’ site in Stade and its structural assembly in Hamburg. The new enterprise would build the forward fuselage of the A330 and A350, the center fuselage of the A320 as well as the rear fuselage and tail cone for all programs. The company is planned to employ 7,000 people in five locations.

These two firms would no longer be considered suppliers to Airbus but instead would be integrated into the Airbus production system and flow. That said, they would remain distinct, separate entities.

The third company would be focused on detailed parts and have an estimated €900 million ($1.1 billion) in annual sales. It would combine the Premium Aerotec sites in Varel with Plant 4 in Augsburg and a facility in Brasov, Romania. Airbus says it is “reviewing different ownership structures to identify the best possible solution” for the parts business. The company believes it can create a strong global player in the detailed parts industry that would be sustainable and competitive with “an appropriate investment strategy.” The newly formed venture could count on a “long-term growth perspective” with Airbus as major customer, the OEM says, but also may work with external clients on civil and defense products.

The company would produce machined, milled and turned parts and have capabilities in metallic and nonmetal components.

The changes identify Airbus’ red line as to what work it is prepared to leave to suppliers and indicate that detailed parts production is not something the manufacturer considers vital in-house work. What they do not address is whether the company’s complex industrial footprint needs a revamp. While no changes are expected—or even possible—in the short term, questions loom on the horizon. The role of Airbus’ plant in Bremen, Germany, has been debated internally for some time, but Faury has not addressed it yet. Airbus also needs to attend to the post-Brexit future of its UK sites at some point, though major changes are only likely when workshares of new aircraft programs need to be decided.

More important than the unlikely prospect of rationalizing its industrial presence across Europe is a side effect of the reshuffling: the strengthening of Airbus’ in-house aerostructures capabilities. Airbus could take on more work itself, and that is a threat for suppliers. According to industry sources, the message from Airbus has already been received by some suppliers that may be directly affected in the not-too-distant future and others that are starting to worry about what the moves could mean for them further down the road.

Two companies that probably have more reason for concern than others are Spirit AeroSystems and Leonardo. Spirit is building the composite center fuselage section of the A350 and the A220 wings, among other things. Leonardo is building the horizontal and vertical stabilizer for the A220. Airbus was about to start renegotiating terms with the A220 suppliers when the novel coronavirus pandemic hit and suppressed production rates. Airbus aimed at significantly better conditions than the A220’s previous owner, Bombardier Aerospace, could reach. Similarly, the A350 is still facing cost pressure, which has only become worse as rates fell to less than five aircraft per month from 10.

According to the industry sources, Airbus has made clear it expects new agreements with its key suppliers in both programs—not just the A220. At the same time, the company has invested massively in new production technology at Augsburg and Nordenham for the A350, infrastructure that is now underutilized.

In the near term, Airbus’ site in Cadiz, Spain, is in focus and that is where the Gutierrez appointment comes into play. The restructuring plan for the Puerto Real plant in Cadiz has been hit hard by the termination of the A380 program and the slowdown of other widebody programs, threatening around 300 jobs there. Airbus “continues to work with the social partners to identify solutions that will optimize the industrial setup,” the company says. Given that Spain has always felt overshadowed in its Airbus role by the much bigger French and German presences, any move is certain to face massive political backlash, even though Cadiz is such a small site.

The topic of facing backlash is something Faury has to keep in mind. Making Airbus a bigger, more centralized entity that covers more of the supply chain also increases risk when things go wrong. For the company, it means tight control over processes is needed. For Faury, who now has upped the game personally, it means he needs to deliver.

Related Content