This article is published in Aviation Daily part of Aviation Week Intelligence Network (AWIN), and is complimentary through Aug 24, 2026. For information on becoming an AWIN Member to access more content like this, click here.

Around this time two years ago, demand was high and uncertainty rife. Heading into Farnborough 2026, some things remain very much the same. Key differences exist, but is it enough to portend a livelier order environment than that of July 2024?

Since last Farnborough, Boeing and Airbus have regained some firmer footing, showing signs of sustained production recovery following several challenging years. Ahead of the 2024 event, Boeing was dealing with fallout from Alaska Airlines Flight 1282 while Airbus fought to recoup supply chain stability from worse-than-expected constraints. Both are now ramping narrowbody production, engine-willing, and pursuing better widebody output. Long-awaited certification of the Boeing 777-9 is making progress, and certification of the 737-7 appears imminent, with the larger MAX 10 variant set to follow. Airbus is hoping to exceed 900 commercial aircraft deliveries in 2026, according to Reuters, above its official guidance of 870.

It would be good timing for growing stability. But war in Iran is a significant, ever-evolving factor, and lingering engine and aerostructure supply chain constraints persist. While volatility has somewhat lost its shock factor at this point in the decade, the Middle East conflict has dinged demand linked to the region and affected some operators more than others. Still, broader demand trends remain encouraging.

“I think we’re all one year smarter and more conditioned to expect maybe the unexpected,” Delta Air Lines CEO Ed Bastian said in January, ruminating on potential risks and macro challenges ahead. And premium consumers, he observed this spring, are “becoming more immune to the headlines and not delaying their investment in the experience economy, waiting to see what the next headline is going to be.”

To his point, persistent appetite for travel has continued through geopolitical disruption, giving carriers cause for some optimism in longer-term outlooks. And as the end of the decade draws closer, so too do critical decisions on aging, less fuel-efficient fleets. Despite near-term headwinds, operators are looking to the future and planning for growth, while also evaluating new and emerging technologies. Strong demand for new aircraft endures, Airbus finds in its recently released Global Market Forecast, and older fleets are accelerating replacement demand. By 2045, nearly 100% of the global commercial fleet will consist of the newest generation aircraft, the airframer expects, up from around 39% today. An ongoing watch item will be whether suppliers can keep up; a double-edged sword as needed boosts to satisfy demand while replacing older jets will strain production but also alleviate pressure on an overburdened aftermarket as retirements increase.

Whether a volume of decisions will be revealed this week is unknown. Analyst orderbook outlooks are not without optimism.

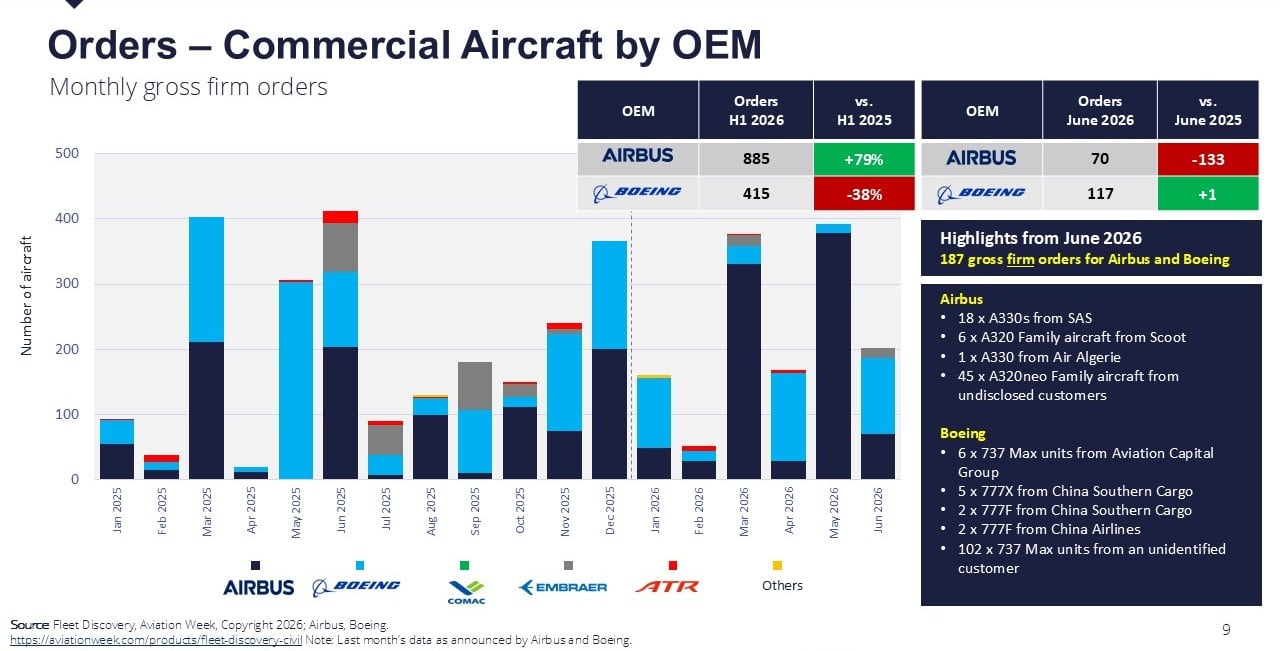

Jefferies analysis sees potential for up to 500 orders this year, commitments it projects could come from American Airlines, Cathay Pacific, Philippine Airlines, Qantas and Singapore Airlines. Looking back, Farnborough 2024’s commercial orderbook came in just shy of 300—when including MOUs, LOIs, and previously undisclosed customer commitments. Tracking only new, firm orders, July 2024’s tally came in under 150 for the full month, according to Aviation Week’s Fleet Discovery database: 89 narrowbodies, 41 widebodies and 13 turboprops.

Where are we now? In the U.S., airlines are planning for fleet transitions as retirements loom. American this summer announced it was actively engaging with both Airbus and Boeing on its next widebody decision. “Given the long lead times associated with widebody deliveries, and expected Boeing 777 retirements in the 2030s, now is the right time to define what comes next,” American Airlines CEO Robert Isom said in June. Both its major rivals have larger widebody orderbooks, including Delta’s two significant commitments announced in 2026. United Airlines has more widebodies on order than its two rivals combined, plus a large narrowbody pipeline. Continuing to renew and upgauge its fleet, United plans to retire “at least” 80 older aircraft in 2027, with accelerated airframer production levels a supporting factor.

Many Asia-Pacific airlines are in the process of discussing aircraft orders, although the timeline of these negotiations and any resulting announcements is uncertain. Philippine Airlines told Aviation Week last year it was considering ordering more widebodies, with a top priority to replace its A330s while also looking to continue the replacement of 777s. Qantas is considering ordering about 20 widebodies—787s or A350s—according to a Reuters report in June, which also indicated that Singapore was in the early stages of discussions for roughly 50 widebodies, potentially 777Xs and A350-1000s. Though Cathay has hinted at the need for further aircraft orders, no timeline details have emerged. Malaysia Airlines also plans to order 16 widebodies, likely in the fourth quarter.

Just prior to the airshow, orders for 95 narrowbody and widebody aircraft were announced by the Air China and Hainan Airlines groups. Air China will acquire 15 A350-900s while subsidiary Shenzhen Airlines ordered 40 A320neos, and in a separate filing Hainan disclosed an order for 40 A320neos. The latter also has orders for 20 A330neo galleys—but is yet to announce any corresponding A330neo commitments. More could be ahead: Boeing in May voiced expectations that further orders from China would follow an “initial tranche” commitment for 200 aircraft.

At the last Farnborough, lower order figures largely came down to timing of big campaigns yet to be finalized, amid uncertainty and disruption. And whether orders are announced sometime this week, year, or decade, industry marches forward. As operators enter the back half of the 2020s, the clock is ticking to secure favorable slots amid unprecedented backlogs.

—with reporting from Adrian Schofield, Chen Chuanren and Sean Broderick

Related Content