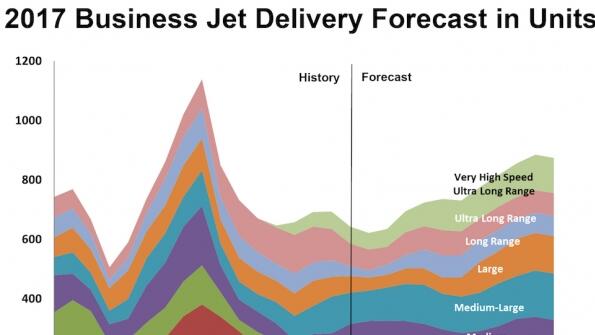

Over the next decade, big-cabin business jets – from super-midsize to business airliner classes – are expected to secure the highest demand, capturing 57% of all global deliveries, according to a just-released forecast by Honeywell Aerospace. Honeywell’s 2018-2027 forecast projects 10-year global...

Subscription Required

This content requires a subscription to one of the Aviation Week Intelligence Network (AWIN) bundles.

Schedule a demo today to find out how you can access this content and similar content related to your area of the global aviation industry.

Already an AWIN subscriber? Login

Did you know? Aviation Week has won top honors multiple times in the Jesse H. Neal National Business Journalism Awards, the business-to-business media equivalent of the Pulitzer Prizes.