Airbus Says Aerostructures Will Remain Core, Gives Cautious Outlook | エアバス社、機体構造分野が引き続きグループの中核事業になるとするも、慎重な見通しを崩さず

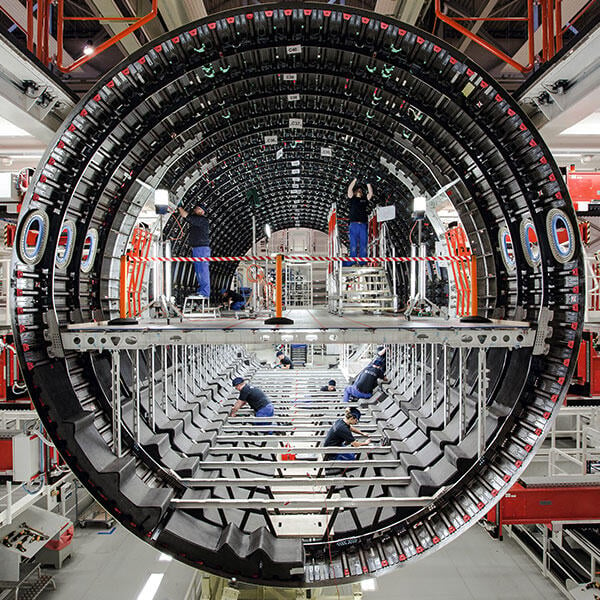

エアバス社が機体構造分野の事業売却を準備してから10年近くなるが、今ではグループ内で長期的に同コンポーネント製造能力を保有し続ける方針に転換した。

2月18日にオンライン開催された同社の年次記者会見で、CEOのGuillaume Faury氏は機体構造分野が「エアバス社のコア事業」であると話した。

エアバス社は2009年初頭、将来的に設計・システムインテグレーション・機体の最終組立に特化することを見据えて、ドイツおよびフランスにあるいくつかの拠点を分割した。しかし、これらの事業部が売却されることはなかった。この時設立されたドイツにある子会社・ Premium Aerotec社はアウグスブルク・ノルデンハム・ファーレルに拠点を保有している。同時にフランスではAerolia社(当時)が設立され、メオルトおよびサン=ナゼールに拠点を保有し、2015年にはSogerma社と合併、Stelia Aerospace社となった。

Faury氏は、現在進められている「デジタル設計・製造・サービス(DDMS)プロジェクト」や、将来機種に想定される要求性能が日々変化していくことを念頭に、「設計と製造を結びつける部分の方がはるかに重要になる」と語った。彼は今後、航空機の機体構造が劇的に変化すると考えており、航空機開発におけるその重要性から、この分野を「社内に保有し続けることが必要だ」と述べた。

一方のボーイング社は2005年に、カンザス州ウィチタにあった機体構造事業部を分割し、Spirit Aerosystems社を設立している。

Premium Aerotec社とStelia社をグループ内に長期的に留め置くという判断は、Faury氏が今後数年間の優先事項と位置づける、ヨーロッパにおける製造基盤をシンプル化していく取り組みにおいて重要な側面を持っている。彼は、両社の再統合をするか否か、するとしたらどのような形で行うのかを明らかにしていない。両社を分割したことは、エアバスグループの目線ではシンプル化に寄与していたが、事業部目線では、売却される可能性を意識した両社がそれぞれ自社の成長を目指していたため、同じ役割を持つ2つの子会社が存在するという無駄が生じていた。

エアバス社による製造基盤の合理化は、Premium Aerotec社やStelia社のみを対象にしたものではなく、グループが保有するヨーロッパ全域の拠点を対象としたものだ。Faury氏は「ヨーロッパ拠点の合理化は多くのポテンシャルを持っている」と話す。ただし、この取り組みでは拠点の閉鎖や、ヨーロッパから中国・アメリカなどへの移転は想定していない。

また同氏は、イギリスのEU離脱後もブロートンおよびフィルトン工場が今後も翼部製造の主要拠点であり続けることを明確にした。

大規模な分割を伴わずにグループ内の製造基盤を効率化するというこの取り組みは、コロナ危機後の需要を見据えた製造レートの調整に向け、エアバス社が取り組んでいる施策の一環だ。しかしFaury氏は、計画の前提条件すら不確実であることから、これは非常に困難なものになると説明している。

彼は生産計画に関して「いま慎重になることが、実際のところ何を意味するのかが分からない」と語る。「短期的には悪化するが、中長期的には改善するように見える。この矛盾をコントロールするのは非常に難しい」と話した。

そうは言いつつも、エアバス社はナローボディ機の生産を徐々に増やしていくという以前の計画を踏襲しており、現在の月産40機から第3四半期には43機、第4四半期には45機に拡大する。「2021年は忙しい年になる」とFaury氏は述べた。

生産数を徐々に増やしていくことは、エアバス社が2022年頃に想定している大幅な増産に向けた準備運動ともいえる。同氏は需要が「2021年よりもはるかに多くなる」と考えているが、ピーク時の月産60機を正当化するにはまだ足りない。しかし彼は、はるかに高い生産レートを可能にする設備とインフラはすでに整っていることから、必要であれば速やかな増産が可能であるとし、ボトルネックになり得るのはむしろ従業員の経験値や効率性だと指摘した。

エアバス社は、航空旅行需要がコロナ危機以前の水準に回復するのは2023〜2025年頃になると今も考えている。Faury氏も「マーケットはコロナ危機以前と似たようなものになる」と考えていることを明確にしたが、環境対策がより重要なテーマになることにも触れた。また「航空機を利用した出張は再開される。あらゆる企業はプロジェクトを再始動する必要があるからだ」と話し、休暇や旅行で「人々は再び飛行機に乗ることを待ちきれずにいる」と続けた。

一方、ワイドボディ機の需要はより長期にわたって低迷するとFaury氏は認めた。現在、月産2機となっているA330neoの製造数を「わずかに」下げる可能性を示唆したが、まだ判断を下す時期ではないとしている。それでも、A330neoはエアバス社のポートフォリオに「長期的に」含まれると述べた。なお、トゥールーズに新設される予定のA321neo最終組立ラインについては現在「凍結状態」だが、「これも再開されるだろう」と話した。

2020年のエアバス社の収益は29%減の499億ユーロ(602億ドル)となり、5.1億ユーロの営業損失、11億ユーロの純損失を計上している。フリーキャッシュフローは73億ユーロのマイナスとなった。

また同社は、受注残の金額を3730億ユーロ(980億ユーロ減)に下方修正した。これにはドルの切り下げなど複数の要因がある。コロナ危機による機材の納入延期やキャンセル分は、減少分のうち10%程度を占めている。

第4四半期には、この年の平均生産数を大幅に上回る機材を納入できたことから、49億ユーロのキャッシュを得た。

2021年には、少なくとも2020年の実績(566機)を上回る民間機の納入を計画している。調整後の税引前利益(EBIT)は今年より3億ユーロ多い、20億ユーロに達するとみられる。また、M&Aおよび利息を差し引く前のキャッシュフローは、少なくとも過不足分岐点は超えると予想されている。しかし、エアバス社CFOのDominik Asam氏は、2021年に10億ユーロ以上の資金調達が必要になる可能性があるしているが、これは輸出信用機関からの強力なサポートにかかっていると述べた。

Aviation Week Intelligence Network (AWIN) のメンバーシップにご登録いただくと、開発プログラムやフリートの情報、会社や連絡先データベースへのアクセスが可能になり、新たなビジネスの発見やマーケット動向を把握することができます。貴社向けにカスタマイズされた製品デモをリクエスト。

Around a decade after preparing to divest its aerostructures businesses, Airbus is now reversing course and wants to keep component manufacturing inside the group for the long term.

Aerostructures are “a core activity of Airbus,” CEO Guillaume Faury told reporters at the company’s virtual annual press conference Feb. 18.

Airbus carved out several of its German and French sites at the beginning of 2009 with a view of divesting them at some point to focus the group on design, system integration and aircraft final assembly. However, the units were never sold. German subsidiary Premium Aerotec includes sites in Augsburg, Nordenham and Varel. At the same time, what was then called Aerolia was set up in France, comprising factories in Méaulte and Saint Nazaire; Aerolia merged with Sogerma to form Stelia Aerospace in 2015.

“The connection between design and production will be far more important,” Faury said. He was referring both to the ongoing move to Airbus’ digital design manufacturing and services (DDMS) program as well as changing requirements forecast with future aircraft models. Faury predicted that aircraft architecture will change significantly and aerostructures therefore will be “an important part” of that process, which “has to remain in Airbus.”

Boeing divested its Wichita, Kansas-based aerostructures business to form Spirit Aerosystems in 2005.

The decision to keep Premium Aerotec and Stelia inside the group permanently will be an important aspect in Airbus’ efforts to simplify its European industrial base, which Faury highlighted as a priority for the coming years. He left open whether and to what extent reintegration of the two subsidiaries will be pursued. Putting their activities in separate units had helped reduce complexity at the Airbus Group level, but it has led to double structures at the unit levels as the two were aiming at building up their own core functions ahead of possible sales to new investors.

Airbus’ industrial streamlining is planned to go beyond Premium Aerotec and Stelia, however, and includes the manufacturer’s primary sites across Europe. “There is a lot of potential for simplification at the European bases,” Faury said. The process is not expected to lead to the closing of any sites or to further outsourcing to bases outside of Europe such as in China or the U.S.

Faury also made clear that UK plants in Broughton and Filton will remain key to Airbus wing production in the future in spite of the fact that the country is no longer part of the European Union following Brexit.

The efforts for a more efficient internal industrial system that is not based on major divestitures is part of a broader exercise of Airbus to adjust to post-pandemic demand and production rates—a process that Faury described as very challenging, even as far as planning assumptions are concerned.

“I don’t know what being prudent actually means right now,” he said referring to production planning. “The short term is getting worse, the mid- and long term looks better,” he said. “That is a contradiction that is very difficult to manage.”

Nonetheless, Airbus is sticking to its earlier plans to begin a relatively slow ramp-up of single-aisle production, going from 40 aircraft per month to 43 in the third quarter and to 45 in the fourth quarter. “We expect a very backloaded 2021,” he said.

The slow increase in production is also seen as a preparation exercise for a much steeper ramp-up that Airbus still believes is likely in 2022. Faury expects demand to be “much stronger than in 2021” but still short of justifying former peak production rates of 60-plus narrowbodies per month. The Airbus CEO pointed out, however, that the company can boost output very fast because the tooling and infrastructure for much higher rates is already in place with staff levels being the key potential bottleneck for a fast expansion of production.

Airbus still expects a full recovery of air travel demand to pre-crisis levels between 2023 and 2025. Faury was also clear in predicting that the market will “be similar to what it was before the crisis,” though the environmental agenda will be much more important. “Businesses need to fly again; they are eager to restart projects.” Also, “people are impatient to fly again” for holidays and on other private trips.

Demand for widebodies will be lower for longer, Faury conceded. He hinted that Airbus may reduce A330neo production “slightly” below the current two aircraft per month rate, though for now it is not making that decision. The A330neo will be part of the Airbus portfolio “for the long term.” The planned new final assembly line for the A321neo in Toulouse is “on ice” for now but is “likely to be restarted.”

Airbus 2020 revenues dropped 29% to €49.9 billion ($60.2 billion). The company made a €510 million operating loss and a €1.1 billion net loss for the full year. Free cash flow was negative €7.3 billion.

Airbus adjusted the value of its order backlog downwards by €98 billion (to €373 billion). Several factors influenced the move, including the devaluation of the U.S. dollar. Around 10% of the reduction was due to aircraft deferrals and cancellations caused by the COVID-19 pandemic.

In the fourth quarter Airbus generated €4.9 billion in cash as it managed to deliver aircraft way above average production rates for the year.

In 2021, the company plans to deliver at least as many commercial aircraft as in 2020 (566). Its adjusted earnings before interest and taxes (EBIT) is expected to reach €2 billion, €300 million higher than this year. And cash-flow before mergers and acquisitions and customer financing will be at least at break-even, according to the outlook. However, CFO Dominik Asam said Airbus may have to finance deliveries of €1 billion or more in 2021, though it is betting on strong support from export credit agencies.