コロナショックによる製造業の再編で、重要度を増す企業規模

もしあなたが航空宇宙防衛(A&D)関連企業の方針に好感を持っているのなら、今後彼らのことがもっと好きになるだろう。数あるトレンドの中で、新型コロナウィルスはA&D業界における触媒としての作用を及ぼすとみられ、大企業が他社を買収し、より多くの受注を勝ち取り、さらなる成長をしていくことになるだろう。

複数の有力者やコンサルタントによれば、今後数年で垂直統合の流れが加速する。主要企業やサプライチェーン最上流の企業は、ここ数十年にわたり自社のプログラムにおける主要業務すらアウトソーシングを進めてきたが、その多くが内製に戻るだろう。

あるアドバイザーは「すでに業界内では垂直統合の動きが始まっており、コロナ危機を乗り越えて行く中で、その一部は加速する可能性がある」と述べている。

ボーイング社は数年前からアビオニクスやニッチな機器の内製化を始めている。昨年はRaytheon社とUnited Technologies社や、L3 Technologies社とHarris 社のような巨大合併があった。当初の目的が収益の確保であれサプライチェーンの維持であれ、今ではコロナ危機によって業界のあり方が変わり、多くの仕事を確保するという新たな目的が生まれている。

Roland Berger社のアドバイザー・Robert Thomson氏とManfred Hader氏は、新規参入の航空宇宙関連サプライヤーはスケールメリットの減少に直面しており、むしろ製造固定費が占める割合が拡大したことで、収益性と競争力が低下するだろうと述べている。内製化と受注拡大による、いわゆるオーガニック売上の拡大は可能ではあるが限界がある。一方、固定費の削減も機器や間接費との兼ね合いから、大きく削ることは難しい。だからこそ、統合という道が重要性を帯びてくる。

つまり、2次請け以下のサプライヤーの財務状況は悪化することになるため、それを持ち上げる機会を作ることが重要になってくる。

トップ企業のCEO達は状況をよく観察している。5月13日に行われた投資家向け説明会で、Honeywell International社の会長兼CEO兼社長・Darius Adamczyk 氏は間もなく転換期が訪れると指摘した。ゴールドマンサックス社に対し「この数年、いかにマーケットが売り手市場であるかを話してきた」「しかし今年後半にはその状況が変わる可能性がある。それは少し買い手市場寄りになり、これまでよりベターかつ違ったものになるだろう。そこに我々は参入したいと考えている」と語っている。

この現象を加速させるものは、信頼性と地政学的な理由からサプライヤーを本拠地に近付けたいという欲求だろう。海外のサプライヤーはその低コスト体質から一時は重宝されたが、パンデミック・経済危機・世界貿易戦争といったリスクに脆弱であることが発覚した。このことから、コンサルタント達は業界の首脳陣があらためて近隣地域に着目すると考えている。

コロナ危機の中でも比較的影響が少ないとされている防衛業界においても、大企業のさらなる拡大が囁かれている。5月13日、Capital Alpha Partners社の常務取締役・Byron Callan氏は「特定の製品に特化するタイプの大企業は、コロナ危機をほぼ無傷で乗り切ることができるだろうが、政府予算の削減を予期しているだろう」「よって、たとえそれがオーガニックグロースではないとしても、2021~25年にかけて成長するには合併や買収が重要になる」と語った。

では、垂直統合やトップからの合併はどこで起きるのか?アドバイザー達のプレゼンによれば、そのヒントはすでに出てきている。まずは、トップサプライヤーの存在がすでに確立しているニッチ製品(フライトコントロールシステム・環境制御システム・降着装置・電気系統・内装)、そして彼らの手がまだ及んでいない領域(メンテナンス・修理・オーバーホール・ロジスティクス・機体構造・エンジン)に注目するべきだ。

次に、トップサプライヤーの視点で供給元を見る。困難な状況におかれていたり、クレジットラインが引き下げられている会社はどこか? そして、民間分野と防衛分野、製品とサービス、旧型機と新型機…など、リスクヘッジが可能になる組み合わせはどれか?といった考え方も有効だ。

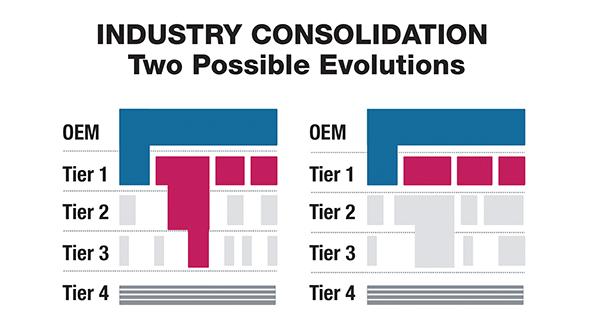

最後に、合併の新たな核になるものが何かを考える。レイセオン社のような「スーパー1次請け」がさらに生まれるのか、2次請け・3次請けの集合体が生まれるのか? Roland Berger社の分析によれば、前者は1次請け~3次請けが持つ細切れの部品生産能力を合理化し、たとえばバリューチェーン全体を管理することで下流サプライヤーの機能不全を防ぐことができる。後者の場合は、業界全体の動きを意識するというよりは、日和見主義的な動きが取られることになるだろう。

あるコンサルタントも話しているが、小規模サプライヤーにとって、この質問はよりシンプルなものになる。買い手になるか、売り手になるか、現状維持のリスクを取るか?たしかに質問はシンプルだが、答えも簡単…というわけではない。

以上は、Michael Brunoが Aviation Week & Space Technologyいた記事です。 Aviation Week & Space Technology は、豊富な経験と人脈を持った専門家により、最新トレンドや最適な状況判断、ポリシー・要求仕様・予算に関する充実した情報を継続的にお届けします。 Aviation Week & Space Technology をもっと知りたい場合、こちらをクリックして下さい。

If you like the cadre of big aerospace and defense companies now, you are going to love them later. Among the major trends the novel coronavirus is expected to catalyze within aerospace and defense (A&D) manufacturing is that the big will get bigger by gobbling up others or taking back more work.

In the next few years, vertical integration should pick up momentum, according to several executives and consultants. After decades of OEMs, primes and top-tier companies outsourcing major work on their programs, many see the pendulum swinging back to bringing more of it in-house.

“We’ve already seen signs of more vertical integration coming through the industry and potentially where some of that could be accelerated as we work through the crisis,” says one advisor.

Boeing started this a few years ago as it insourced avionics and other niche segments. Major consolidation picked up last year with the mergers of Raytheon and United Technologies Corp. and L3 Technologies and Harris Corp. Now, whether it be protecting profits or securing supply, the reasons to own more of the work are burgeoning as industry is refashioned in the COVID-19 crisis.

For starters, aerospace suppliers are facing diminished economies of scale but a greater share of fixed-cost in production, with a likely loss in profitability and competitiveness, say Roland Berger advisors Robert Thomson and Manfred Hader. So-called organic top-line increases, through insourcing and acquisition of additional work packages, are possible but only to a limited degree. A fixed-cost reduction likewise is only feasible up to a certain level due to equipment and overhead structures. So consolidation is an important lever to consider.

Part and parcel to that will be the financial distress into which suppliers in Tier 2 and below fall—and the opportunity to roll them up.

Top CEOs are watching. Speaking May 13 to an investor conference, Honeywell International Chairman, CEO and President Darius Adamczyk cited an inflection point. “For a couple of years now, I’ve been talking about how it is a seller’s market, not a buyer’s market,” he told Goldman Sachs. “But that calculus may change in the second half of the year, and I think it could become a bit more of a buyer’s market, and the valuations may be better and different. That’s something that we want to partake in.”

Feeding the phenomenon could be a desire to bring supply closer to home, both for reliability and geopolitical reasons. Suppliers overseas once were revered for their low-cost footprint, but suddenly they are seen as vulnerable to pandemics, economic stress and global trade wars. In turn, consultants expect industry leaders to take another look at favoring local regions.

Even in the defense realm, which for now is considered safer during this downturn, there is talk of larger firms becoming even more powerful. “Large pure-plays should come through the pandemic relatively unscathed but may be looking at lower spending growth outlooks,” Capital Alpha Partners Managing Director Byron Callan noted May 13. “Mergers and acquisitions may thus be more important in delivering growth—even though it’s not organic growth—in 2021-25.”

So where to look for vertical integration and consolidation from the top? Clues are already emerging, according to advisor presentations. First, look at niches where top suppliers already are prevalent—environmental and flight-control systems, landing gear, electrical power and interiors—and others where they are not there yet, including maintenance, repair and overhaul, logistics, aerostructures and engines.

Next, look at the supply base from the perspective of a top supplier. Who is distressed or drawing down credit lines? What revenue mix do certain potential targets have—e.g., commercial vs. defense, products vs. services or aging vs. next-generation platforms?

Finally, consider where the new nucleus of consolidation will be. Will more “super Tier 1s” such as Raytheon Technologies emerge, or will conglomeration occur among Tier 2 and 3 providers? The first would allow rationalization of capacity for detailed part production from Tier 1 to 3, for instance, with the super Tier 1s able to secure through-value-chain control and prevent subtier supplier failure, according to Roland Berger. The latter likely would be opportunistically driven rather than following any overarching industry logic.

For smaller suppliers, the questions are more concise, as one consultant says. Do you want to be a buyer, a seller or risk it as is? A simpler question, for sure, but no less difficult to answer.