Interview: COVID-19's Impact On The Global Civil Aviation Industry

In a May 20 interview conducted by Lin Zhi Jie, China Business Network CBN’s Contributing Editor and CARNOC’s Columnist, Paul Burton, Managing Director Asia-Pacific of Aviation Week Network, shares his thoughts on a range of issues around the impact of the COVID-19 crisis on the global civil aviation industry.

1. The COVID-19 crisis is now a global pandemic. What is the impact on the civil aviation industry? Which countries are most affected and which are relatively less affected? Why?

With the peak in COVID-19 cases having passed in many Asian countries, several are looking to introduce creative ways to lift travel bans.

From China and South Korea’s easing of quarantine requirements in 10 Chinese regions and three cities for some pre-approved business travellers, to Australia and New Zealand’s creation of a ‘trans-Tasman’ travel bubble – this would mean that quarantine-free travel allowed between Australia and New Zealand, governments are starting to use inventive techniques to re-open the skies.

That said, the recovery of international air travel takes much longer than that of domestic air travel, with the opening of borders likely to proceed in a phased-in manner.

EUROPE

European airlines are still reeling from the impact of the COVID-19 crisis, but the need to look ahead toward a post-coronavirus future to determine how the region’s air transport industry will evolve in the longer term is clear.

Even airlines that were performing well before the coronavirus crisis are looking for external help. The goal is to ensure they survive long enough to take advantage of an anticipated increase in passenger demand when widespread travel restrictions are removed.

British Airways (BA) has set out plans for a major restructuring and redundancy program as a result of the COVID-19 pandemic, with up to 12,000 people leaving the airline.

Lufthansa Group’s immediate financial situation remains unclear after the group rejected proposed conditions on a €9 billion German government bailout package. Senior executives at Lufthansa believe the airline can operate around 50% of a normal schedule in the upcoming winter timetable, at best.

Norwegian Air Shuttle, which was already under financial pressure following rapid expansion before the COVID-19 crisis grounded nearly all of its fleet, has warned that without more state help it will run out of cash by mid-May. The airline plans to focus on tried-and-tested routes—such as long-haul flights between London and New York or London and Los Angeles, or intra--Nordic services in the short-haul network. It will also look to put in place a cost-cutting initiative and drive an increase in ancillary revenues.

The Air France-KLM group, which has grounded 90% of its fleet since the crisis began, is also looking to the future, with the help of a massive bailout from France and the Netherlands.

ASIA

In Asia, markets such as South Korea and Vietnam are following China with signs of growth in domestic flights, although the fact that schedules are still shrinking in other countries such as Indonesia and Japan show a region-wide improvement remains elusive.

Domestic air travel is generally expected to rebound sooner than international demand in most countries, as internal travel limitations will be lifted before border restrictions. China has already demonstrated this trend with an increase in domestic capacity over the past few months.

South Korean carriers are now beginning to reinstate services on the country’s small but busy domestic network. Korean Air cut 60% of its domestic seat capacity in April compared to a year earlier but expects to have a smaller reduction of 52% in May.

Until April 28, Korean Air was operating just 36 daily domestic flights, with only six of its 17 routes operating. However, by May 18 it expects to be flying 59 daily flights on 15 domestic routes. It will also operate 15 routes during the April 29-May 5 holiday period.

Vietnam is the latest Asian market to show signs of a domestic travel recovery. Government restrictions meant that Vietnam Airlines was at one point reduced to operating just a single daily flight on the Hanoi-Ho Chi Minh City route, previously one of the busiest in the region. It was only operating two other domestic routes, with three flights a week each.

Vietnam has garnered praise from other countries for the effectiveness of its response to the coronavirus, and the government has progressively allowed domestic flights to increase. Data from Aviation Week Network’s CAPA – Centre for Aviation (CAPA) and OAG shows that Vietnam Airlines’ domestic seat capacity bottomed out in early April before starting to rebound. Rival VietJet shows a similar pattern.

The picture is bleaker in other markets. Japanese domestic capacity has not yet rebounded, and Japan Airlines has seen its flight reductions climb from 37% in early April to an estimated 68% by May 10. All Nippon Airways has also cut its domestic flights by 70% as of April 28.

Indonesia’s domestic market had been less affected than many other countries in the region. However, this situation changed dramatically on April 24, when the Indonesian government banned scheduled passenger services until June 1. This is part of a move to restrict the traditional visits to hometowns during the Ramadan and Eid periods, with fears such mass movements could spread the coronavirus. The government has said the end date will be extended if necessary.

Whether airlines are cutting or reinstating domestic flights depends on where their home country is in terms of the coronavirus cycle. Some of the initially worst-affected Asian countries are now recovering best, while other countries are yet to see the peak of the outbreak. The examples of emerging growth at least show there is light at the end of the tunnel for Asian airlines.

2. Moving on to a global level, the COVID-19 has severely affected the global economy and IMF predicts a 3% decline in global GDP in 2020. How long do you think it would take the global civil aviation industry to return to pre-coronavirus levels?

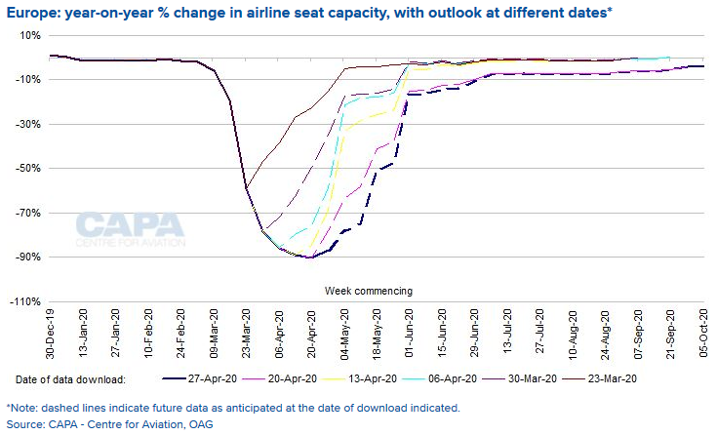

Initial projections around a V-shaped recovery as followed 9/11, SARS and the global financial crash are now proving less likely. Here is some data from CAPA showing the current forecast in Europe:

3. Many countries have implemented a lockdown. As a result, video conferencing has become a norm for many people working from home. In China, the “Live broadcast of the Forbidden City tour " has gotten 400,000 viewers. After the epidemic, will cloud office systems, cloud conferences and cloud tourism become a new way of life? If so, will people still travel like before?

It is my contention that those accustomed to travel for business or leisure will want to return to the skies as soon as possible, either to reconnect with clients or their favourite beach/restaurant! There may be a consolidation around the corporate travel sector, where companies that have been forced to utilise virtual meeting software realise that internal meetings with attendees from multiple countries and continents are no longer essential.

4. It is not easy for airlines to survive this crisis with low cash flow. Some governments have lent a helping hand by providing aid like guaranteed loans, paid wages, capital injection, airline subsidies and tax relief. But there are also those who leave companies to their own survival. Which approach do you think works best, has the greatest value, and is worth learning from?

The situation is fluid, and changes from country to country. Unfortunately, there is no one size fits all solution to these complex situations, and domestic politics, economic priorities and often intangible sensitivities from key players combine to ensure an intricate patchwork of approaches.

For instance, in the U.S., at the time that legislators passed the USD2 trillion Coronavirus Aid, Relief, and Economic Security (CARES) Act, airlines and labour unions alike hailed the legislation as a breakthrough for the portion of the bill that pledged approximately USD25 billion in payroll grants to the airline industry for sustaining worker pay and benefits until the end of September 2020.

But a last-minute provision in the bill attached major strings to those payroll grants – allowing the government to take an ownership stake in airlines that sought both the payroll grants and loans included in the financial relief package.

Unions are decrying the move, and the nation’s airlines are now attempting to negotiate with the US Department of Treasury on the terms of the grants as collectively they continue to burn through nearly billions of dollars in cash each day. Labour is warning that the longer Treasury drags its feet, the higher the risk of painful bankruptcies will continue to grow significantly.

Meanwhile, Virgin Australia’s decision to enter voluntary administration has thrown the future of the carrier up in the air. However, this process could yield a more viable roadmap for a major player in the Australian market.

The intention of Virgin and the administrator is to relaunch with as much of the airline intact as possible, but the ultimate shape of the carrier will also depend on its new ownership.

Virgin was driven to its knees by the COVID-19 pandemic, which has destroyed demand. This occurred at a bad time for Virgin, as its new CEO was embedding strategic changes aimed at improving its financial performance.

It has been forced to put its plans at the mercy of an administrator, creditors and potential new owners. Virgin’s management has proposed its existing business plan as the best way forward, but there is no guarantee that this approach will be accepted.

Of course, many other airlines around the world are also facing the need to restructure for a post-COVID demand environment, and are scrambling to refinance. The difference with Virgin is that much of the control over the transformation process has been taken out of its hands - although the Australian government has inserted a prominent banker to act as a sort of guardian of the national interest.

5. The civil aviation is among the hardest-hit industries in the COVID-19 crisis. How can Aviation Week Network help?

The Aviation Week Network has helped to keep our industry abreast of global developments during every major crisis since we launched the first edition of Aviation and Aeronautical Engineering on August 1, 1916, in the middle of the World War I.

And today — more than at any point in our history — the Aviation Week Network is uniquely positioned to help the world’s aviation community make sense of seemingly overwhelming challenges.

Recent additions of CAPA, ASM and Routes to our team mean that we have the entire information spectrum covered in all regions, from daily news to detailed analysis from the industry’s most experienced and connected team of experts, a unique portfolio of data and forecasts and all forms of face-to-face and digital events. The Aviation Week Network can help the industry through the coming weeks and months supporting situational awareness, critical decision making and, ultimately, a return to growth.

We are committed to action and are introducing more robust ways for the market to know, predict and connect as we all navigate the crisis and position for the future.

As leader of the business in Asia, I am proud of our accomplishments in helping to establish a solid base in China and other key countries around the region. We now produce more content in Mandarin, Japanese and Korean than ever before, and are now very active on WeChat and Weibo.

6. The Boeing 737 MAX has been grounded for more than a year. Recently, it halted commercial aircraft production because of the COVID-19 crisis and was forced to abandon the acquisition of Embraer. Would Boeing enter bankruptcy reorganization? Would the federal government step in to help Boeing?

On April 30, Boeing filed regulatory notice that it could raise an undetermined amount of new debt financing through newly issued bonds, coming a day after the company’s chief executive outlined a grim outlook, albeit better than feared by the marketplace.

Boeing has not specified how much it could raise in new bonds in the Securities and Exchange Commission prospectus it filed, although Aviation Week believes that it could seek $20-25 billion.

That would come on top of a nearly $14 billion credit facility Boeing drew down in mid-March as COVID-19 spread around the world. Total debt was $38.9 billion as of the end of March, up from $27.3 billion at the end of 2019.

Boeing said the notes will be issued in multiple parts with maturities ranging from 2023 to 2025, 2027, 2030, 2040, 2050 and 2060—so the latter entailing a 40-year bond. “We intend to use the net proceeds from this offering for general corporate purposes,” according to the prospectus.

The prospectus came a day after Boeing CEO and president David Calhoun and CFO Greg Smith told analysts and reporters that the embattled OEM, already suffering from the total halt of its 737 MAX narrowbody, saw a pathway to returning to pre-pandemic growth in three-to-five years. Boeing stunned Wall Street and the aerospace world in March when it openly asked for at least $60 billion in federal aid for itself and its suppliers as passenger air traffic collapsed from the coronavirus outbreak.

In teleconferences held on April 29, the executives asserted liquidity concerns have eased since then, thanks to the U.S. government passing the CARES Act with its corporate loan and grant programs, as well as a separate but related program at the U.S. Federal Reserve to backstop corporations.

Calhoun and Smith outlined options to tap a mix of financing sources to meet Boeing’s needs. They did not provide details, and they acknowledged it would take longer to repay growing debt with changed aviation industry dynamics.

Several Wall Street firms have estimated that Boeing could be headed for total debt around $45 billion.

Access authoritative market insights and locate new business with access to company, program, fleet and contact databases - only available with AWIN. Sign up for a free demo today.

Related Content