The 737 MAX-related layoffs had already begun before 2019 was over. Aviation Week’s Wichita bureau chief says smaller suppliers near 737 aerostructures provider Spirit AeroSystems started cutting their workforces around the Air Capital of the World before New Year’s Eve, and not because of usual holiday shutdowns.

This was not how the commercial aerospace sector expected to enter 2020. A year ago, suppliers were talking about not being able to hire enough workers to keep up with Boeing’s 737 monthly production rate increases, planned to be at least 57 new aircraft by now.

Fast forward, and the specter of layoffs is likely to be a leading topic of conversation around boardrooms and dinner tables, from Wichita to Chicago to Seattle, let alone the countless smaller municipalities that are home to hundreds of suppliers on the halted narrowbody program. With Boeing and Spirit shutting down their respective 737 manufacturing lines indefinitely this month, a nightmare scenario is turning into reality.

Through the holidays, companies have been practically silent, ostensibly because the optics of negative comments were bad, and also due to self-imposed quiet periods before the release of 2019 financial results starting at the end of this month. But they are also struggling to work out exactly what the production stoppage and new leadership at Boeing all means and whether there will be financial aid from the OEM or governments. Nevertheless, industry observers are increasingly clear the impact will be widespread and bruising.

“The suspension of production will have far-reaching adverse consequences for the broad aerospace and defense supply chain,” a team of analysts at Moody’s Investors Service say in a report issued Dec. 23, the same day Dennis Muilenburg was fired as Boeing CEO. “Reduced activity related to the 737 MAX—one of the biggest aircraft programs by volume globally—will precipitate lower revenues, earnings and cash flows, and slow the growth in operating profits that we had previously anticipated for 2020 under the former assumption that the MAX grounding would end in January.”

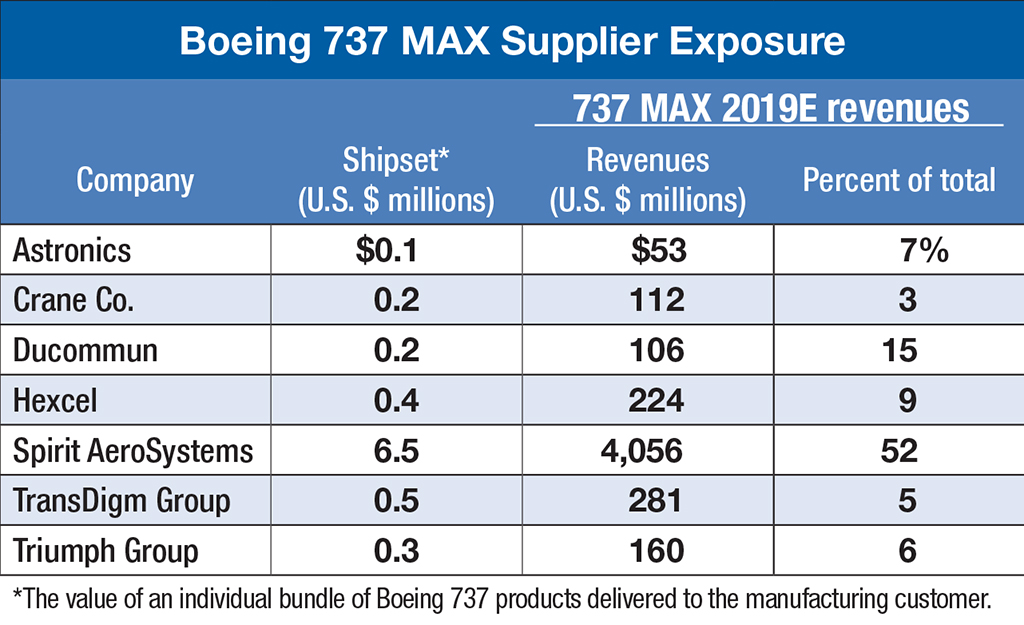

CNBC celebrity stock picker Jim Cramer was more blunt a few days earlier. He says production halts suppress the whole aerospace manufacturing sector and likely mean 2020 forecasts across industry will have to be cut or, at the least, weighted to the back half of the new year. “Honeywell? Yes. Spirit, TransDigm, those will be hurt,” Cramer opines. “But I think we have to revisit the earnings per share for United Technologies and GE, and these are companies that have been great suppliers to Boeing. I’m waiting for big revisions down.”

While the MAX is down, it is not out, and there is still blue sky in long-term forecasts. Yet analysts do not see the commercial aero sector normalizing until 2021 at the soonest. As for 2020, whatever happens, it will be darker than what many expected just a month ago.

A 2020 forecast issued Dec. 18 by Moody’s called for 6% profit growth, including Boeing’s, but that assumes the MAX’s grounding does not last beyond mid-year.

Rival Fitch Ratings also calls the MAX’s return critical. “The impact of the MAX suspension should be temporary unless substantial orders are canceled,” the credit agency said Dec. 19. “Our rating case assumes the MAX groundings will be lifted in phases by different regions through early second-quarter 2020 and that deliveries in various regions will resume shortly afterwards.”

However, the long-term impact of the MAX grounding on the aerospace sector is likely to be negative due to growing regulatory scrutiny, the ratings agency adds. New aircraft certifications will take longer and became costlier for manufacturers, while regulatory actions in case of difficulties are likely to be faster and more rigorous.

Others agree that the MAX freeze augurs worse-than-before results for A&D in 2020. “We can expect a negative ripple effect across the aerospace industry in 2020,” Accenture Global A&D Lead John Schmidt tells Aviation Week. “This impact is likely to be more significant than prior rate reductions because of the complexities facing suppliers in restarting idled production lines back up to full production rates.”

In October—when Boeing still was promoting a MAX return to service by year-end—Schmidt’s group had already halved its expected growth forecast for global A&D in 2019 to just 2.5%. Rival Deloitte projects commercial aircraft order cancellations and lower-than-expected new orders in 2019 likely meant total airliner production was cut to around 1,450 units. Airbus and Boeing should issue their tallies imminently. But while the coming weeks should bring a lot more information for the sector, there likely will be even more questions.

Related Content