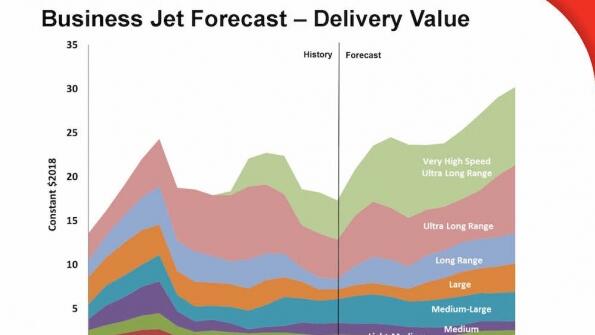

New business jets entering service will help drive robust short- and medium-term growth in the industry, which also is seeing a tightening market for used jets, Honeywell Aerospace finds in its annual Global Business Aviation Outlook. Honeywell predicts manufacturers will deliver 7,700 new business...

Subscription Required

This content requires a subscription to one of the Aviation Week Intelligence Network (AWIN) bundles.

Schedule a demo today to find out how you can access this content and similar content related to your area of the global aviation industry.

Already an AWIN subscriber? Login

Did you know? Aviation Week has won top honors multiple times in the Jesse H. Neal National Business Journalism Awards, the business-to-business media equivalent of the Pulitzer Prizes.