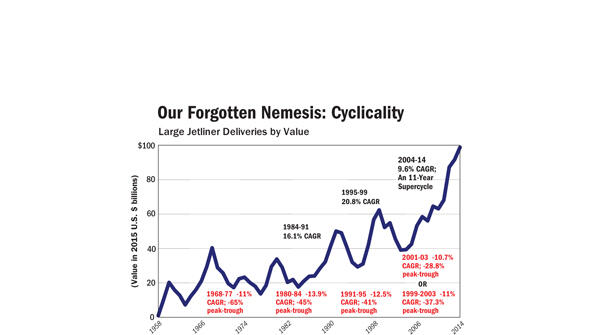

The jetliner supply chain might find itself the victim of someone else’s idea of success. As both Airbus and Boeing consider a further ramp-up of their A320 and 737 single-aisle jetliner families, everyone involved should consider the likely ramifications. Talk of higher rates has been increasingly...

Subscription Required

This content requires a subscription to one of the Aviation Week Intelligence Network (AWIN) bundles.

Schedule a demo today to find out how you can access this content and similar content related to your area of the global aviation industry.

Already an AWIN subscriber? Login

Did you know? Aviation Week has won top honors multiple times in the Jesse H. Neal National Business Journalism Awards, the business-to-business media equivalent of the Pulitzer Prizes.

Related Content