Forecast Focus: GE Aerospace North American Commercial Engines

GE Aerospace engines currently power over 72% of all North American widebody aircraft and are forecast to power over 78% by the end of 2034. North American commercial engine MRO over the next 10-years is forecast to account for over 46% of the total North American commercial MRO demand. GE Aerospace engines will make up 39% of the total engine MRO spend for North America totalling $52 billion in MRO demand over the decade. Engine MRO demand for GE Aerospace engines is anticipated to grow by just over 4% in total, and show a modest CAGR of .5% according to Aviation Week’s 2025 Commercial Aviation Fleet & MRO Forecast.

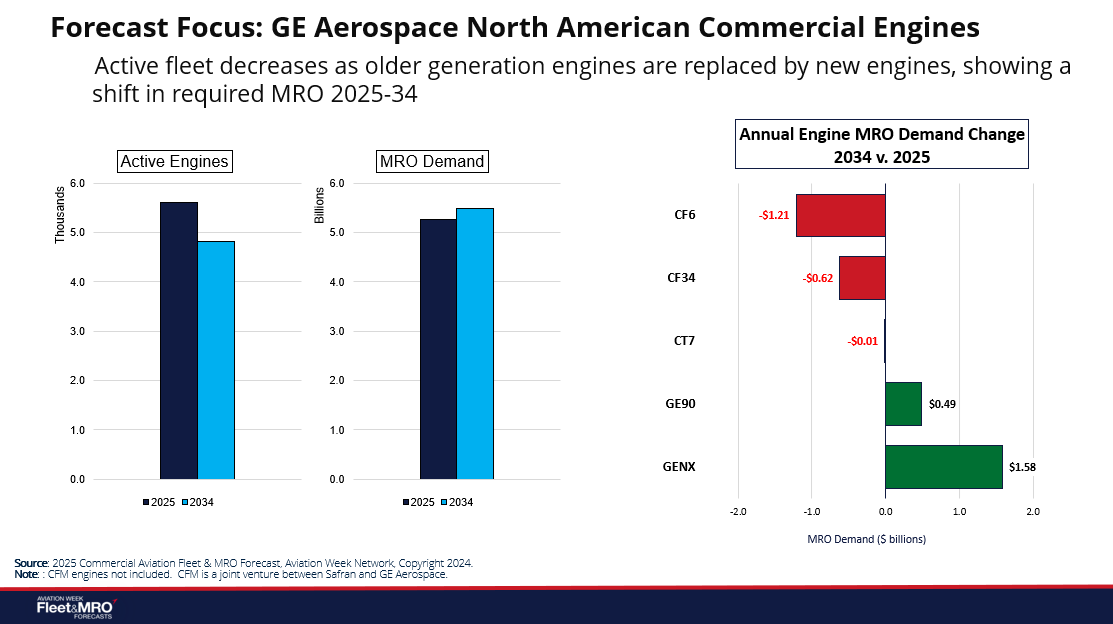

The active GE Aerospace commercial engines for North America are anticipated to decrease from nearly 5,600 active engines in 2025 to just over 4,800 active in 2034. This decrease in the active engine fleet does not translate directly to a decrease in MRO demand as required MRO is expected to increase by over $225 million during the same period.

GE Aerospace engine MRO demand will be dominated by the CF6 engine family, capturing over 35% of the total demand, followed by the CF34 engine family at 22% and GENX engine family at 22%. However, by the end of the forecast period, the GENX family is projected to require the majority of GE Aerospace engines MRO yearly demand. GENX engine population more than doubles from 2025 with approximately 610 engines to nearly 1,300 operating engines in 2034. With an estimated $745 million in demand for the active GENX engines in 2025, these engines account for just 14% of the total GE Aerospace engine MRO for North America. By 2034, the estimated MRO for the GENX engine family should account for over 42% of this MRO demand, increasing to over $2.3 billion, a 210% increase.

GE Aerospace North American Commercial Engines