CAPA Perspective: Factors that will determine the speed of corporate travel recovery

Business and corporate travel is vital for airlines. Corporate travel accounts for 10%-15% of airline passenger numbers, yet provides roughly 20% to 30% of airline revenue, depending on the carrier. For some airlines, it accounts for up to 75% of profits. Corporate bookings at Lufthansa Group, for example, accounted for 45% of revenue pre-pandemic.

Citibank did a study in 2020 that showed a 1% impact on global corporate travel volumes has a 10% drop impact on global airline profits. Last year, corporate travel spending dropped 51.5% and it is far slower to recover than leisure travel.

In 2019, total global spending on corporate travel was $1.43 trillion, according to the Global Business Travel Association. It accounted for 21% of global travel and tourism, and contributed 1.5% of global GDP. It had been growing at an average pace of around 3.5% in the five years prior, 2015-2019, and China and the US accounted for nearly 45% of global total business travel spend. But growth had slowed to just 1.5% in 2019.

Between April 2020 and the end of the year, global travel spending for business travel fell 68%, a massive difference compared with previous downturns. After the 9/11 attacks in 2001, business travel spending fell 11% and it fell 7.5% in the wake of the global financial crisis in 2009.

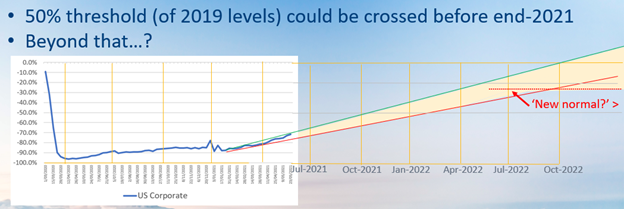

So far this year, data from China show a full domestic traffic recovery, back to 2019 levels, but US business travel is still down by around 70%, even though domestic leisure travel is close to a full recovery.

Drawing a line from the start of this year, bumping along the bottom of the trend, it looks as though the industry might cross a 50% threshold of global business travel volumes before the end of 2021, led by domestic China and domestic US. Beyond that, it's really anyone's guess.

Clearly, open borders are going to be essential for international business travel to recover, along with vaccination rollouts, but there are some factors that could help speed recovery. GDP and economic growth are key drivers of business travel. Encouragingly, the Organisation for Economic Co-operation and Development (OECD) has lifted its 2021 global GDP estimate from 4.2% to 5.8%.

We keep hearing about strong pent-up demand for travel and for companies to restore in-person meetings. Airline, hotel and travel executives say there is growing evidence of a need for face-to-face interaction with customers. This will be a potential driver of near-term recovery, assuming that borders and movement restrictions do not get in the way, especially after the northern summer and as businesses return to offices. The NGO sector, sports travel, government sector generally, resources and pharmaceuticals appear to be leading corporate travel recovery. Small and medium-sized enterprises are also at the front of the recovery.

There's also some conjecture that the decentralized and flexible work arrangements could lead to potentially more commuting by air. And there is talk about rebooted travel programs by corporates with an emphasis on employee duty of care that will remove some of that hesitancy from travelers and get them back on the road.

Summing up these factors in their potential importance to a shorter or longer business travel recovery, it looks like this:

● Borders reopen on vaccination success: Essential for international travel

● Strong GDP growth: Critical

● Strong pent-up demand: Very high

● Sale/competition and face-to-face meeting: High

● Decentralized/flexible working: Medium

● Rebooted travel programs focused on employee care: Medium

Airlines have had to shift and pivot to rely more on cargo revenues and the visiting friends and relatives/leisure segments. All eyes will be on the post-northern summer period for evidence of further recovery in the US domestic business/corporate travel market. Much will depend on it.

Related Content