CAPA: The Resilience Of Middle East Hubs

Airlines operating in the Middle East are more heavily dependent on international traffic flow than many other parts of the world. This is mainly because of the absence of significant domestic air travel markets in many countries. There are some exceptions, of course, with Saudi Arabia being the standout, and as the feature in this issue highlights, there are bold ambitions for the country to further boost its global standing in the air transport sector (see page 14).

Talk of the region has been dominated recently by the full-service intercontinental operators and how quickly demand will recover to pre-pandemic levels to support their business models. However, as in other regions of the world, LCCs have also been adapting to the changing market and growing their own point-to-point networks.

Their success in what remains a challenging environment is helped by having a strong and efficient airport infrastructure to support their revival. Airports across the Middle East have been challenged by border closures and market accessibility, and while the Middle East has been successful in both curbing and battling the pandemic, it faces the same recovery hurdles seen across the globe.

The reliance on international traffic, which has been slower to recover from the troughs of the pandemic than domestic demand, has raised many questions over the future of the major Middle East gateways, which had previously transformed global air travel in and out of the region, but also via, particularly on busy Europe-Asia routes.

IATA data for 2022 show Middle Eastern airlines saw a 157.4% traffic rise in 2022 compared to 2021. Capacity increased 73.8% and load factor climbed 24.6 percentage points to 75.8%.

The nature of the networks of its biggest airlines meant the region delivered the strongest year-on-year growth in both RPKs (144.4%) and ASKs (67.0%). While annual load factors were in the mid-70%s—below the 80%+ recorded in North America, Europe and Latin America—they were up almost a quarter versus 2021 (23.9%). It was the region with the biggest year-on-year rise, with levels down just 0.7% from 2019.

Return to Profit

What is different about the 2022 and 2023 markets versus before the pandemic is that pent-up demand and continued supressed capacity mean air fares have risen and airlines are now reaping benefits. That may not compensate for the losses from 2020 and 2021, but certainly supports business recovery.

Dubai-based Emirates Airline posted a record first-half net profit for the six months ending Sept. 30, 2022, of AED4 billion ($1 billion) compared to a loss of AED5.8 million for the same period the previous year. Abu Dhabi-based Etihad Airways also delivered a profitable performance in the first half of 2022, supported by an ongoing transformation effort.

IATA expects airline profitability to return in 2023 for the region’s carriers after cutting net losses from almost $5 billion in 2021 to around $1.1 billion last year. In 2023, passenger demand growth of 23.4% is expected to outpace capacity growth of 21.2% and generate profits of $268 million for the region’s airlines. Over the year, the region is expected to serve 97.8% of pre-crisis demand levels with 94.5% of pre-crisis capacity.

Middle East carriers are well on the way to restoring pre-pandemic activities following the lifting of COVID-19 restrictions. The region has benefitted from a certain degree of re-routing resulting from the war in Ukraine, and more significantly so from the pent-up travel demand using the region’s extensive global networks as international travel markets have reopened.

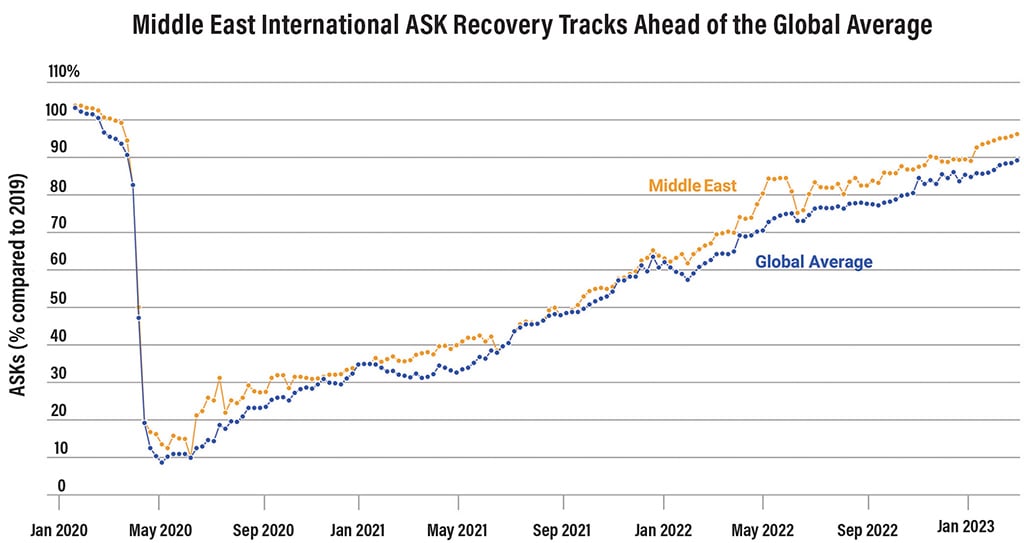

CAPA data show that Middle East international ASKs have tracked ahead of the global average throughout the worst of the pandemic and during the subsequent recovery phase. This continues a trend that was evident ahead of the health crisis.

International ASKs across the Middle East only declined to single-digit percentages versus pre-pandemic for a single week (9.8% for week of May 25, 2020) as airlines such as Qatar Airways continued to fly while many others across the world were grounded. In fact, for a time the Doha-based airline was the world’s largest by flying capacity.

By the middle of June 2020 international ASKs in the Middle East were back above 25% of pre-pandemic levels, but it wasn’t until September 2021 that they had passed the 50% level. Since then, there has been a steady climb, with levels surpassing the 90% rate consistently through the early months of 2023.

A return to some degree of air travel normalcy has seen Dubai International Airport once again return to the number one international airport position by both capacity and traffic.

The region’s major airlines have also returned their largest capacity airliner, the Airbus A380, to operational service despite many predicting the permanent grounding of the aircraft early in the pandemic. However, flight cycles of the twin-aisle widebodies that are the backbone of Middle East operators remained at around 85% of pre-pandemic levels as of January. In comparison, narrowbody jets recovered to equivalent 2019 levels in summer 2022, and utilization has remained above those levels since.

As is normal for the industry, one that has more than its fair share of crises, numerous headwinds remain and the growth of Saudi Arabia’s international aspirations will put increasing pressure on the region’s airlines and hub airports. But they have already shown strong resilience in overcoming the crisis and will retain a key role in facilitating regional and global connectivity.

Related Content