Travelers navigate a security checkpoint at Denver International Airport in November before the US Thanksgiving Day holiday.

Back in the black, but with razor thin margins. Costs rising. Crowded planes and airports along with congestion, flight delays and lost bags. It’s good to be back to business as usual, even if that means dealing with the same old problems before a virus took air transport chaos to an entirely new level.

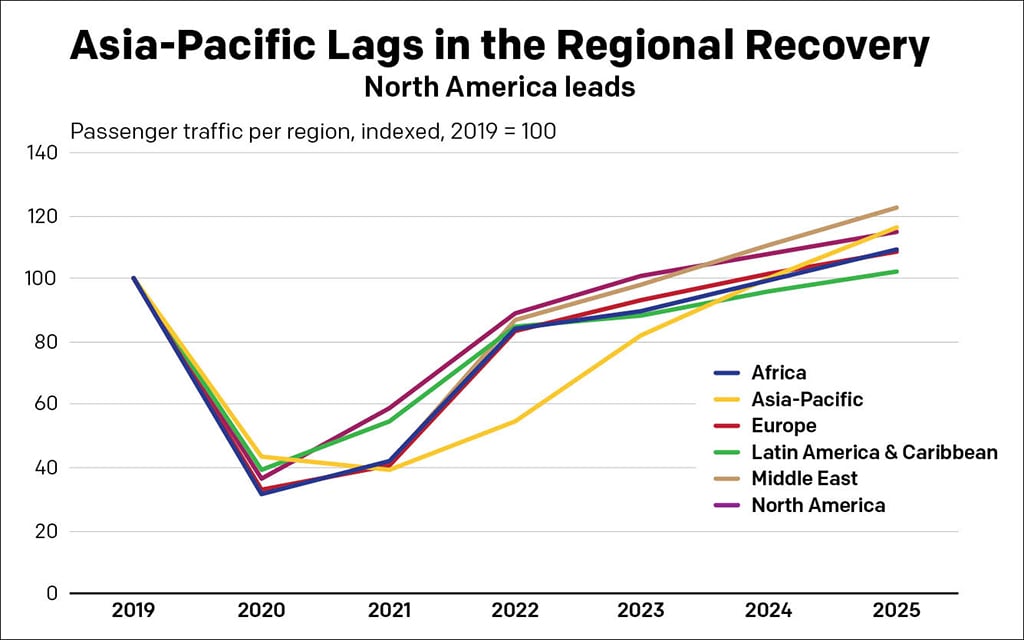

The world’s airlines as a collective will return to profitability in 2023, IATA expects, but the net profit will be miniscule and some major regions, including Asia-Pacific, will remain in the red.

Subscribe to the best-read publication for the global airline management community: Air Transport World magazine. Written by Air Transport World’s expert team of journalists, every article focuses on what airline management professionals need to run their airline.

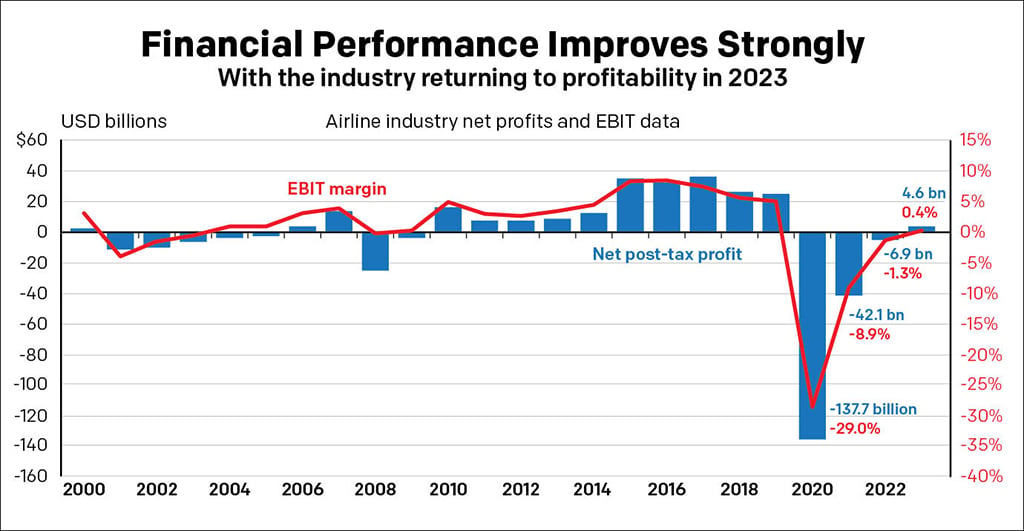

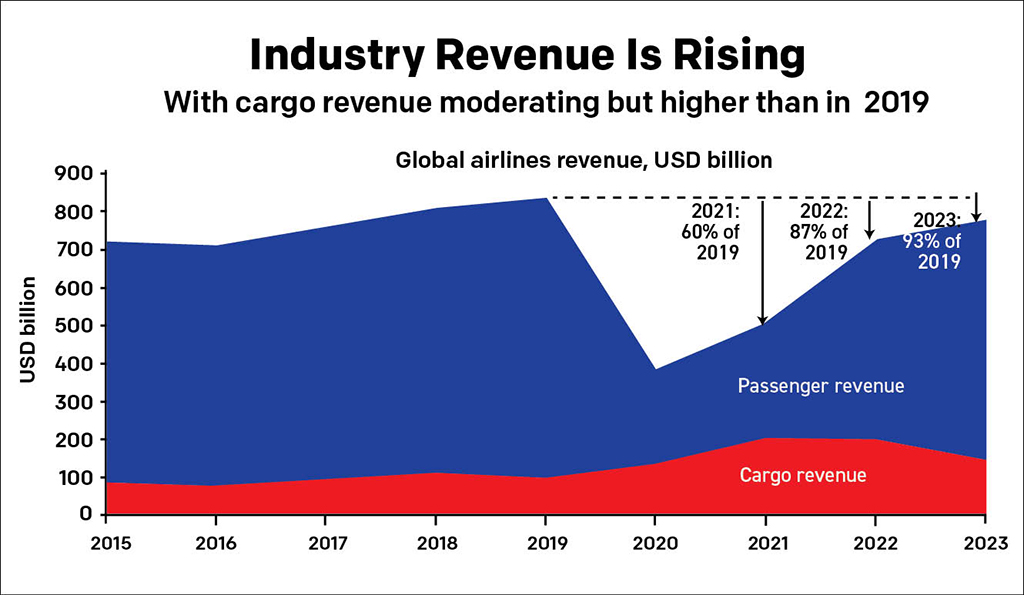

IATA released its 2022/2023 forecast in mid-December from its Geneva headquarters. Global airline net losses for 2022 are expected to be $6.9 billion on revenues of $727 billion—an improvement on the $9.7 billion loss forecast in June and significantly better than the $42 billion loss in 2021 and $137.7 billion loss in 2020, the first year of the pandemic.

For 2023, IATA forecasts airlines will collectively post a $4.7 billion net profit on revenues of $779 billion. While a significant milestone, marking the first profit since 2019 when the industry posted a $26.4 million net profit, the margin will be just 0.6%, showing the continued financial fragility of the industry. Costs, meanwhile, are expected to grow by 5.3% to $776 billion.

“There is much more ground to cover to put the global industry on a solid financial footing,” IATA director general Willie Walsh said. Nevertheless, Walsh said he was optimistic going into 2023. “The headwinds we face are significant, but I would describe them as business-as-usual headwinds. We still have positive economic growth and while I’m an optimist at heart, I think I am also a realist,” he said.

REGIONAL OUTLOOKS

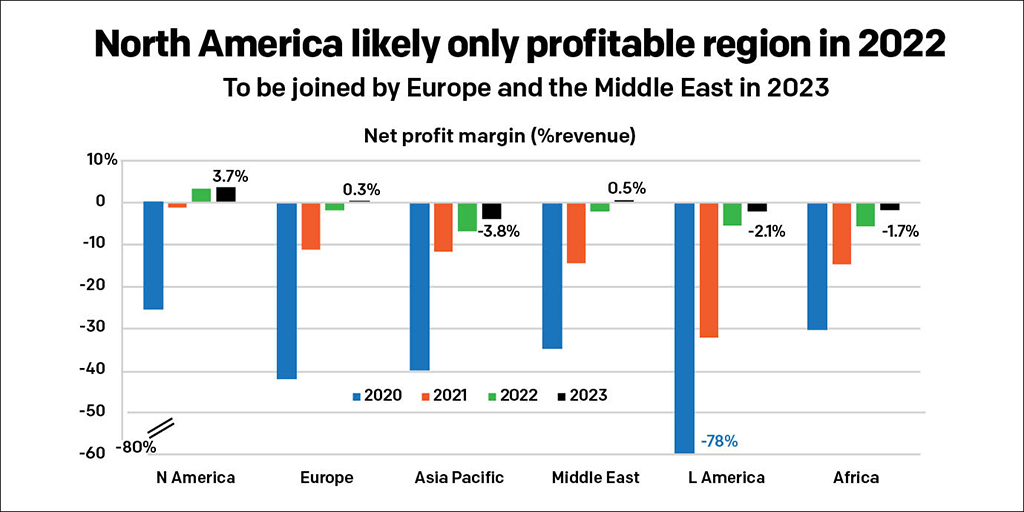

The timelines for profitability return vary from region to region, with North American carriers ahead of the curve and the only ones expected to realize profits in 2022. Overall, IATA anticipates North American carriers will see a profit of $9.9 billion in 2022 and $11.4 billion in 2023. The large US domestic market and the reopening of the transatlantic market have boosted the financial position of American carriers.

The next two regions that are expected to return to profit will be Europe and the Middle East, IATA predicts. European carriers are expected to see a loss of $3.1 billion in 2022, transitioning to a $621 million profit in 2023. In 2023, passenger demand growth of 8.9% is expected to outpace capacity growth of 6.1%. While the war in Ukraine has curtailed activities of some carriers, direct impact on the industry is limited. The much bigger effect is how the war has pushed up oil prices.

Middle East carriers are expected to post a loss of $1.1 billion in 2022 and a profit of $268 million in 2023. This is another region where demand growth, at 23.4%, will likely outpace capacity growth, at 21.2%, in 2023.

Latin American and African carriers will remain in the red through this year and in 2023. For Latin America, the collective net loss is expected to be $2 billion in 2022, reducing to $795 million in 2023. For Africa, the 2022 loss of $638 million is expected to reduce to $213 million in 2023.

Asia-Pacific remains the region with the bleakest financial outlook. IATA expects to see carriers there post a loss of $10 billion this year and $6.6 billion in 2023. While many countries in the region have reopened their borders this year, China’s zero-COVID policies and travel restrictions are having a significant drag on the overall region, although some easing of those policies at the end of the year—when Hong Kong also lifted all its COVID travel restrictions—gives cause for optimism in 2023. Even so, IATA believes Asia-Pacific will not return to profitability until 2025.

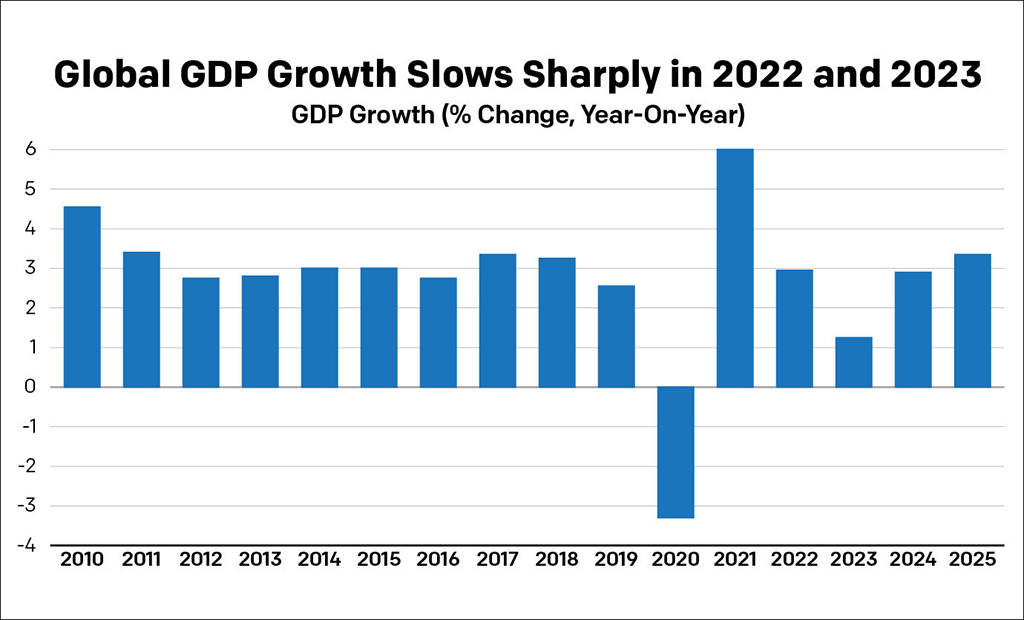

IATA chief economist Marie Owens Thomsen noted that outside influences on airline fortunes include a sharply slowing GDP, from 3% in 2022 to an anticipated 2% in 2023, which economists regard as recessionary. However, Owens Thomsen also described it as an unusual “job-rich economic slowdown,” which helps insulate the effects.

“We expect this to change sometime in 2023, but as more people are employed than ever before, it’s underpinning growth,” she said.

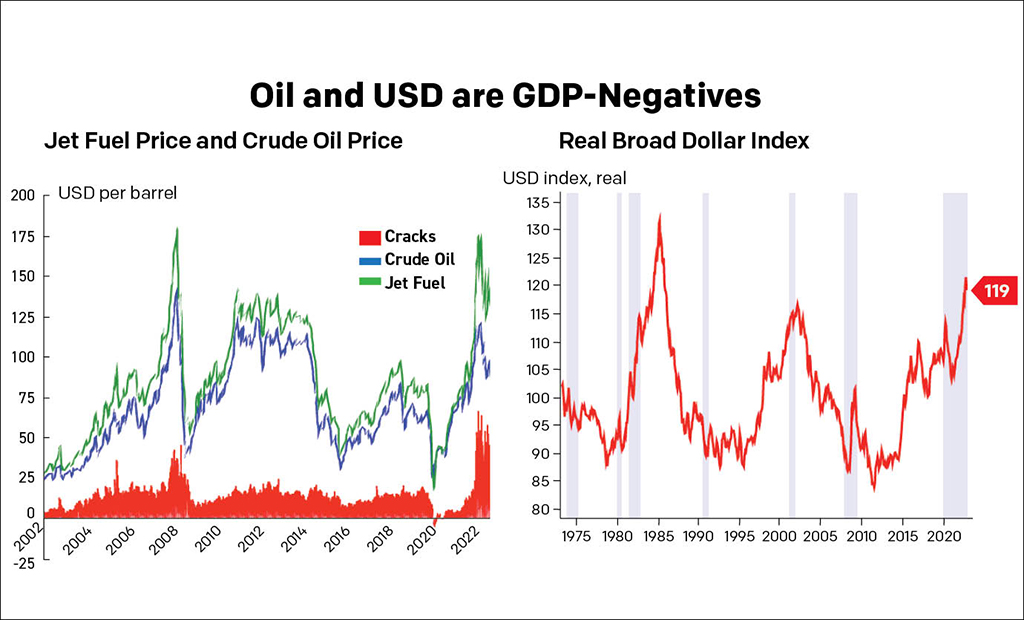

The high price of oil, and in particular a historic crack spread—the premium paid for jet fuel versus Brent crude—is another influence. Total airline fuel spend for 2023 is expected to be $229 billion, or 30% of expenses. That is based on Brent crude costing $92.3/barrel and jet kerosene averaging $111.9/barrel.

Walsh warned that even where profits are returning, they are “razor thin,” while costs—particularly for fuel and related to 2050 carbon net-zero emissions goals—will increase significantly.

“Revenues have to reflect the increase in costs,” he said. “This is not an answer that a lot of people want to hear—that is, if oil prices continue to go up as the industry transitions to net-zero, then ticket prices will have to reflect that, but ultimately we will have to pass on the costs.”

In a podcast interview with ATW, Owens Thomsen noted that IATA’s projected industry profit of $4.7 billion in 2023 “is on the one hand an absolutely stunning and phenomenal performance because the loss that the industry experienced in 2020 was completely unprecedented, never seen before. I don’t know what words to use to impress upon everybody how absolutely exceptional that was, and it was not far off a $140 billion loss. So, that we managed to recover within the space of four years—given the magnitude of what happened in 2020—is really quite extraordinary.”

The recovery, she said, was “completely driven” by travel restrictions or the absence thereof, that replaced all the standard macroeconomic models typically used for predicting traffic volumes.

“In a sense, developments are a bit divorced then from the macroeconomic evolution, which is after all not super great. We’re going from 6% growth in 2021 to barely 3% this year, and maybe barely 2% to next year,” she said. “So it’s interesting to see how that has not influenced traffic flows because it’s all about can we travel or can we not travel?”

This favored US airlines, which were quickest to return to profit, because the US reopened its borders early and its very large domestic market never closed.

“We can see other countries too that have benefited from a similar approach. Mexico, for instance, has also done really well in a situation where they did not impose very many restrictions, if any,” Owens Thomsen said.

WAR AND PEACE

Elsewhere, Europe’s challenges include the war in Ukraine.

“It has to be said that the most growth-promoting policy that we can put into place anywhere is peace. So, while it looks today as if it would take a miracle for the war to end soon, if it could end, it would obviously help us greatly, both globally and for our industry, in that energy prices could come down, food prices could come down, the US dollar appreciation could be somewhat thwarted, and all of those things would clearly help both the global economy and our industry,” she said.

“Even if the countries bordering on Ukraine do not represent a very high percentage of the total global air traffic, their connectivity is extremely important to them. They now have a lack of air connectivity. They do not have a rail system that is as developed as Western Europe’s rail system, and arguably the same could be said to some degree regarding road transportation and so on. We calculated at some point that an increase of 10% in connectivity in Europe could bring about a long-term gain in GDP in Europe of a percentage point. So, if we are looking at economies that are sort of tethering on the brink of recession and we think about what kind of impact this lack of connectivity is going to have, that’s obviously quite dramatic.”

CHINA'S GLOBAL IMPACT

A key factor in the speed and consistency of the recovery will hinge on what happens in China next year. Beijing’s zero-COVID policy has impacted China’s domestic air travel market—which briefly overtook the US in 2020 to become the world’s largest—and international markets, especially those in Asia-Pacific. The beginnings of a lifting of some restrictions at the end of December hinted there may be more change to come in 2023, but there remains much uncertainty.

“We do think that the traffic volumes in China will not reach the 2019 levels before 2025. Obviously, it’s very hard to know how policies will pan out, but our current assumption is that it will be eased progressively throughout 2023, perhaps with an emphasis on the latter half of 2023,” Owens Thomsen said.

“But even as we come to the end of next year, we do not think that all restrictions will be removed. So, we’re seeing a very slow progression there. And, of course, any delay to that slow progression is only going to delay the traffic recovery to the year at which it might reach 2019 levels.

“There are other countries in the Asia-Pacific region that are doing much better, but they are nevertheless deprived of the Asia-China traffic. So, it does also affect their own performance. But for sure, other countries have opened up more and are doing better than China in the Asia-Pacific region. But given the size of the Chinese market, it sort of skews the conversation in an unfortunate way, but still one that makes sense given the magnitudes.”

OUTSIDE INFLUENCES

Looking to other influences outside the control of airlines, but which directly affect demand for air travel, and therefore profitability, Owens Thomsen plays down the talk of a global recession.

“I think that the public uses the word recession in a too liberal manner, and we are not expecting a global recession at the current junction,” she said.

“There are actually not that many global recessions. It’s unfortunate that we just had two in quite rapid succession, the other global financial crisis and the one associated with the pandemic. But before that it was the Great Depression. So, global recessions don’t happen that frequently. It could happen, indeed, if China remains in lockdown for longer than what we are currently assuming. We’re not saying that it’s a zero risk, but it’s not our base case scenario.

“However, maybe about a third of global GDP countries put together could be affected by some form of recession, so obviously we’re looking at minus 10 or something in Russia, minus 13 in Ukraine, and we can expect recessions in Germany and the UK and a number of other countries. This is why the importance of China again comes to the fore, because if we are not seeing much growth engine being provided by Europe and the US, and the Chinese growth engine goes into neutral, then indeed we could be flirting with some very low numbers if China doesn’t come back.”

Another uncertainty—an age-old one for airlines—is the state of the oil market.

“The oil market is notoriously volatile and it’s a market that produces very large price swings in response to very small variations in supply and demand; that’s always been the case,” Owens Thomsen said.

“Now those price swings are likely to be exaggerated, given the war in Ukraine, and notably because there will be an embargo against Russian energy exports from the European side, to be implemented on Feb. 5. And the challenge then becomes for the Europeans to try to obtain that energy from somewhere else, which is also extremely difficult.

“In total, we expect to see a price spike around February. But as a trend, I do still think that we have seen most of the oil price inflation and we should guard against how we react emotionally to these spikes. The average oil price tends to surprise people as a rule because we remember the big numbers. We don’t really expect to see that much more average oil price inflation, but we also don’t necessarily think that it’s going to drop by any phenomenal amounts, so it will probably remain in the vicinity of a 100 [dollars per barrel of crude], or 90 to a 100 on average next year.”

Overall, Owens Thomsen says the industry’s ability to come through the pandemic crisis is a positive that shows its continued resilience. But she worries about what she calls its robustness.

“I have huge respect for the excellent crisis management of all our airlines. But the issue that the industry is still lumbering with is robustness. If we think that resilience is the ability to stand up again once you’ve been knocked over, then robustness is the ability to not fall down in the first place. And that would be clearly very helpful to our industry,” she said.”

Related Content

Comments