Commercial Aerospace At A Crossroads: Balancing the Present and the Future

Contributors: Frank Coleman, Henry Marcil, and John Moore – McKinsey & Company

The commercial aerospace sector faces a historic backlog of aircraft orders and anticipated demand for new-build current-generation aircraft. As it ramps up to satisfy these the industry is also on the cusp of developing and fielding Next Generation Single-Aisle (NGSA) designs - the centerpiece of air transport for decades to come.

A survey of leading firms in the commercial aviation supply chain indicates they are unsure of whether they can meet market demand for current platforms in a timely fashion. They are similarly uncertain of what investments they’ll need to make to realize NGSA and the long term strategies for commercial and partnership models which go along with it. This calculus is complicated by larger forces outside the industry from uneven economic growth to a volatile global geostrategic environment.

McKinsey partnered with Aviation Week to survey 175 leaders across more than 80 firms ranging from airframe and engine OEMs to suppliers, MROs and operators on key questions as to how they will respond to the challenges of meeting current demand while tooling up (figuratively and literally) for future aircraft and technologies.

Their responses reflect collective uncertainty and differing perceptions not only of the future of the industry but also how to prepare for it. Any of three different directions can be taken at a crossroads and, similarly, industry faces a trio of unresolved questions about how it will go forward.

Despite the lack of immediate answers, we see a roadmap for the sector to be successful in tackling both the near-term ramp up and “landing” in a place where the industry is healthy enough to deliver the NGSA.

Uneven Demand, Differing Production Perceptions

Today, commercial aerospace occupies what - at face-value - appears to be an enviable position.

The post-Covid production backlog has grown to an all-time high. At the end of March Boeing’s backlog of unfilled orders had swelled to a record of over 6,000 aircraft, a new company record, 75% of which were narrowbody jets. Airbus reported a backlog of more than 8,600 aircraft (also a record) 90 percent of which were narrowbodies.

Given the full order books, projected wait times to receive a new-build aircraft currently hover around a decade assuming 2023 delivery rates. The industry expects demand for new aircraft to grow at an estimated ~8% CAGR through 2027. From 2024 through 2030, this suggests on the order of 12,000 jets are expected to be delivered.

However, these growth and delivery projections, as always, are subject to trends in commercial traffic. Annual air passenger traffic growth rates are expected to recede to more normal levels as the industry moves away from the Pandemic period. This trend is forecast worldwide and especially in the Asia Pacific region which has been a significant driver of industry growth in recent years.

Observers may also note that production growth has failed to recover to the levels anticipated pre-COVID. The now familiar story of supply chain disruption has been driven by challenges such as a dearth of skilled workers, constrained supply of all manner of components, geopolitical stresses and accompanying inflation.

Facing a confluence of headwinds and tailwinds (large backlog, uncertainty in near-term demand, continued supply chain and operational challenges, and ample excitement about the next generation of narrowbody jets), our survey asked three fundamental questions for commercial aerospace to consider:

- Is the industry on track to reach the production ramp-up projections espoused by airframers for current narrow-body platforms?

- What do survey respondents believe are the greatest challenges facing development of a next-gen single-aisle aircraft, and when will the NGSA reach market?

- In context of both the production ramp up of existing platforms and NGSA, what is needed to ensure a healthy and financially strong value chain? Should we expect today’s business models to transfer directly to the NGSA?

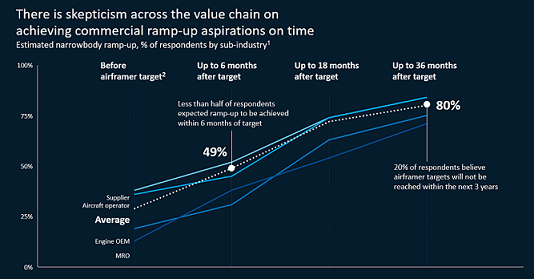

Over the past 24 months airframers have communicated a narrowbody production ramp-up to be achieved in 2026-2027. Yet there was speculation as recently as the first-quarter of this year as to whether the targets they articulate can be achieved given the aforementioned supply chain production challenges and managed production slow-downs.

These challenges likely underlie reporting that airframers are carrying extra inventory to shore up supply chain risks. In fact, Airbus revised its ramp-up guidance in late June to delay by one year.

In that respect it is not surprising that survey respondents predicted a ramp-up delayed by 8-12 months on average; with 30% of respondents believing targets will be missed by 18 months or more. A further 20% of respondents believe the ramp up rate targets will not be reached within 36 months of the OEM targets which we interpret to effectively mean that one in five respondents don’t believe the ramp-up will be achieved at all.

Moreover, the survey finds that 65% of suppliers indicate their current production systems are inadequate to reach airframer ramp-up targets, suggesting a potential gap in production, plant and equipment (but also likely labor) which suppliers and airframers will need to jointly determine how to fill. The shortfall is most pronounced in engine suppliers and Tier 2 suppliers.

The push-pull tension between airframers and suppliers is not new. As far back as 2021, airframers were asserting that planned production rate increases were strongly supported by customer demand and arguing that they needed more buy-in from a supply chain reluctant to come in fully behind the expansion. The survey response shows that some elements of this tension remain.

The revised ramp-up schedule that Airbus announced in June changes the game – both in underscoring the need for real action by suppliers & airframers, but also for airlines to recognize that they may need to adapt their fleet planning. Older aircraft are likely to remain in service longer - increasing demand for leased assets, aftermarket services and parts.

Summarizing, the supply chain’s view on ramp up is clear - the commercial aerospace sector is not yet on track to reach the airframer production ramp-up targets.

Mixed Messaging & NGSA

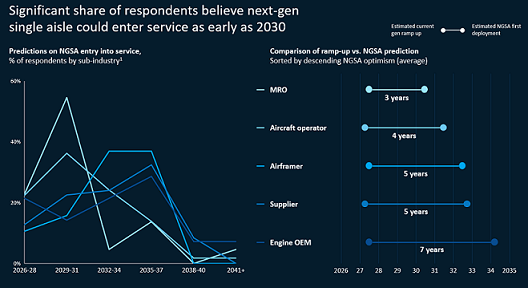

Perhaps the most surprising finding of the survey is an incongruity between the aforementioned doubts about the production ramp-up and relative optimism about the arrival and entry into service of next generation single-aisle platforms.

84% of respondents predicted an NGSA deployment in 2035 or prior.

Initially, it is hard to see how the same group of respondents can be so pessimistic about production ramp yet optimistic about NGSA, which revolves around similar constraints. However, the contradiction begins to make sense as one dives deeper into the results. It hinges on how the NGSA is defined.

The survey reveals a close correlation between each respondent’s prediction about the technological sophistication of the NGSA versus its entry into service date. Much has been made about the application of new designs and new technology from transonic truss-braced wing (TTBW) and blended wing body (BWB) airframe concepts to hybrid-electric, hydrogen-combustion or fully sustainable aviation-fueled (SAF) propulsion systems.

Despite this, most respondents expect a conventional tube-and-wing design (with increased use of composites) and an improved (but conventional) gas turbofan propulsion system.

Recent reporting and analyses also support this notion. NGSAs may essentially represent re-winged (composite) variations of current designs, possibly with open rotor engine architectures but certainly containing evolutionary advances in engine core design and materials. A more conventional combination is achievable on a shorter timeline, consistent with the relatively optimistic survey results.

Respondents predicting more advanced airframe technologies such as TTBW or BWB designs expect NGSA deployment 18 months later on average than those predicting conventional tube & wing designs. Design and technology choices obviously bear on potential entry into service but there is a notable disconnect in opinion about NGSA timing between systems integrators and the aftermarket, and propulsion and component providers.

Airframers and MROs are the most optimistic with more than half of respondents estimating an NGSA deployment by 2030. On the other hand, just 25-35% of suppliers (engine and non-engine) see NGSAs in place by then. This suggests a gap between what suppliers truly believe they can deliver, and their public communications (or lack thereof).

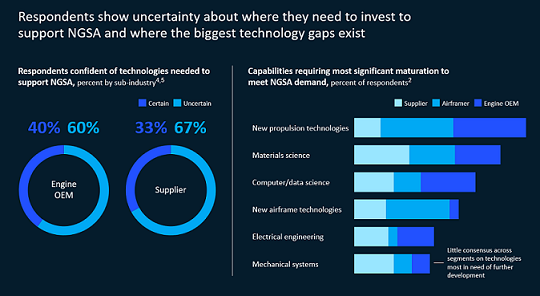

Optimism and pessimism on entry into service is closely aligned with self-reported R&D investment. Airframers report they are investing approximately 65% of their R&D capital in next generation aircraft, while engine OEMs and suppliers are investing considerably less – as little as 20%. The disparity may be linked to indications of uncertainty on the technology requirements for NGSA.

Over 60% of suppliers reported they weren’t sure of the R&D priorities to support the NGSA – due in part to lack of clear guidance from airframers on which technologies will be front and center.

It is also worth mentioning that at both airframe and engine OEMs, engineers are being diverted away from NGSA development to solve issues with current programs. This diversion could have a negative impact on timing regardless of the technology inputs being considered for any particular NGSA configuration.

The lack of clarity is more pronounced (and more potentially impactful) for more advanced technologies. If the industry is serious about disruptive propulsion (such as hydrogen) in the 2030’s, communication with suppliers is needed in short order to ensure the right R&D efforts are being made. The more ambitious the change, the greater the challenge – in research, new and evolved supply chains, and infrastructure – required to realize it.

In summary, the more optimistic view on NGSA telegraphs a less ambitious view of what the industry believes the NGSA is most likely to be – a compromise between technology, risk, and ultimately performance. For the industry to make a bigger bet, airframers and suppliers must collaborate closely on the technology roadmap.

Commercial Models & Near Term Priorities

The commercial aerospace value chain has struggled to fully recover from the COVID pandemic and the fallout revealed weaknesses in current commercial models (e.g., unforeseen risks of production slow-downs, inflation, and labor shortages) which have not yet truly been solved.

We believed that suppliers would want major changes in their relationships with airframers and Tier 1s when looking forward to the NGSA but instead what we found is that most respondents haven’t yet fully thought through what lies beyond the near term challenges they face.

Our survey asked about the commercial and partnership terms suppliers and airframers were most interested in asking for and offering, respectively. We then applied a “zone of potential agreement” framework to identify areas where the wishes of suppliers and airframers about future commercial agreements potentially overlap.

Over the last decade, many supply agreements in commercial aerospace carefully defined terms which essentially attempted to forecast the future. Despite efforts to build in flexibility they simply could not foresee everything – and those gaps turned out to be more serious than anyone could have anticipated.

Standing at the other extreme are partnership-focused arrangements with risk and revenue sharing partnerships (RRSPs) in the engine market serving as an archetypal example.

These and other partnership-type agreements have the potential to create substantial upside for suppliers, sharing of risk for airframers, and greatly reduced need to write contracts which contemplate all future outcomes. It is not a free lunch of course, as these arrangements introduce risk beyond a supplier’s own control both in the program’s commercial success and in the performance of counterparty suppliers.

Our analysis reveals that in the near term both airframers and suppliers showed a desire and a willingness to provide clearer demand signals and volume guarantees, inflation protection, and working capital support.

Airframers in particular expressed openness to this, even a willingness to offer higher margins to suppliers to incentivize participation in the production ramp-up. When we asked the same question about priorities for NGSA commercial and partnership models, we anticipated different answers but in fact, the results were strikingly similar (emphasizing inflation protection and working capital support).

This may be an indication that suppliers are content with the commercial partnerships on current programs but in our view it is more likely that suppliers writ large are focused on the challenges of today and struggling to think beyond.

The potential implications of this are significant. While the challenges to meet the production ramp up are real, airframers and suppliers must not miss the natural opportunity the NGSA provides to select partners and reset the commercial model. Firms who have a clear strategy – whether airframers or suppliers – have the potential to exploit a significant first mover advantage.

Thus, the third question we asked going into our market survey – what changes to business models are needed to ensure a financially strong value chain - is left not fully answered, and remains a topic which will need to be considered carefully by the industry over the next 1-2 years.

A Crossroads and a Roadmap

The commercial aerospace industry is undoubtedly at a crossroads. The competing priorities of expanding current-gen production and turning the supply chain to NGSA will require both significant investment of capital expenses and R&D, respectively.

Given the widespread belief that the production ramp-up will be delayed, there exists a risk that these demands on resources will overlap. We anticipate many firms will struggle to generate sufficient cash to fulfill both.

The first challenge is the investments required to meet the ramp-up. While airframers have a clear business case to accelerate deliveries, extant suppliers may face step-changes in costs when production is forced to scale beyond their current assets, and in the medium term may worry that they are scaling their own production beyond what others in the supply chain can deliver. A single supplier may not have strong incentives to invest now, especially if they are not confident these assets will convey to the NGSA.

On R&D, the challenges lie in uncertainty in which technologies to pursue and timing. In the last 15 years we have seen R&D cycles for clean-sheet aircraft which can easily reach a decade or more; suppliers indicated limited confidence in the specific technologies they need to invest in. (They also indicated that less than one third of their current R&D is being allocated to new programs).

If the views from our survey on the NGSA’s entry into service (84% predicting EIS by 2035) are to hold, R&D will need to accelerate and our results suggest this is likely to require airframer guidance. It may take time for the industry to recognize and admit that R&D is not yet on track for any of the more ambitious technologies.

However the likelihood that NGSA looks more like an evolution from current technologies rather than a revolutionary design can potentially mitigate both of these risks.

We see a roadmap wherein industry can meet both its current-gen ramp up and near to mid-term NGSA priorities.

It begins with near term actions to secure production expansion including meaningfully increased transparency between airframers and suppliers, willingness by both parties to invest in production pinch points, and commercial support in the areas identified by the survey (volume security, inflation protection and working capital assistance). From there, airframers and suppliers both will be better positioned to tackle the real challenge of execution.

These steps, while important, only get industry through the next 12-18 months. Each firm must define its NGSA strategy and with it the commercial models & partnerships required to realize it.

Will the future reflect the supplier construct of the past, or should it move to a greater emphasis on partnership, mutual investment, and risk sharing?

We believe airframers and suppliers who win will be the ones who:

- Are most transparent, treating their value chain as partners rather than solely customers and suppliers.

- Have the most clarity about their long-term strategy and which elements of their commercial strategy from current generation-platforms need to change to make that a reality.

- Are those who manage effectively through the “messy middle” as current-gen platforms sunset and the NGSA ramps up.

While none of these choices are easy, ultimately the future of the industry will turn on whether airframers and suppliers choose to focus on the current generation, the next generation, or can effectively manage to achieve both.

Those who do this most effectively will enjoy many advantages because they’ve made the most important choice when facing a crossroads – deciding which direction to take.

For more information, listen to our Podcast: Can Airbus And Boeing Win Back Suppliers' Confidence?

Related Content