A&D Companies Rushed To Send Shareholders Cash In 2014

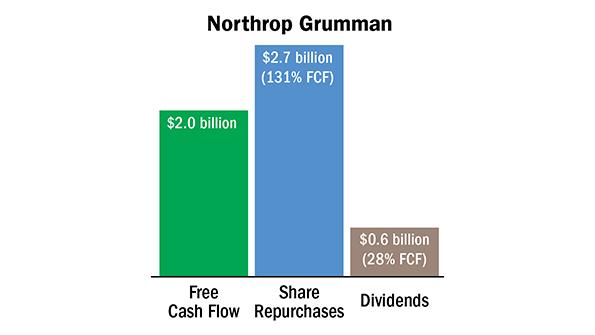

Shareholders in aerospace and defense have never had it so good. The largest publicly traded companies in recent years have generated billions of dollars in free cash flow, as defined by operating cash flow minus capital expenditures, with most of it returned to shareholders in the form of dividend...

Subscription Required

This content requires a subscription to one of the Aviation Week Intelligence Network (AWIN) bundles.

Schedule a demo today to find out how you can access this content and similar content related to your area of the global aviation industry.

Already an AWIN subscriber? Login

Did you know? Aviation Week has won top honors multiple times in the Jesse H. Neal National Business Journalism Awards, the business-to-business media equivalent of the Pulitzer Prizes.

Related Content