Rapidly Developing Technologies in the Future of Elevated Mobility

Authors: John Coykendall, Matt Metcalfe, Aijaz Hussain, and Tarun Dronamraju

Introduction

After years of false starts and pilots, advanced air mobility (AAM) is finally emerging as a viable mode of transportation to carry people and goods in new, community-friendly, and cost-effective ways. 2021 was a milestone year for the AAM market as electric vertical takeoff and landing (eVTOL) aircraft companies witnessed $5.8 billion in investments.1 In contrast, eVTOL companies registered $4.5 billion in investments between 2010 and 2020.2 Furthermore, Joby Aviation3 was the first company to go public, followed by Archer,4 Lilium,5 and Vertical Aerospace.6

AAM is emerging as a significant shift in mobility, offering fundamentally new capabilities and applications that were previously not feasible. With urbanization and population growth driving congestion in cities, AAM promises to save passengers time, improve productivity and quality of life, increase accessibility for rural and disadvantaged communities, and expand access to goods and services. Trips using AAM could take minutes instead of hours as in the past.

Manufacturers aim to see eVTOL flying by 2024,7 and the AAM industry could become mainstream in the 2030s as companies strive to make it a commercial success.8 According to Vertical Flight Society, approximately 600 eVTOL aircraft concepts and designs are being developed by about 350 companies worldwide.9 At the same time, the healthy competition between eVTOL companies could help evolve the AAM ecosystem more efficiently and rapidly.

This article examines where and how AAM can compete with the existing modes of transportation and focuses primarily on the consumer perspective given the available options.

Can AAM enhance the transportation ecosystem?

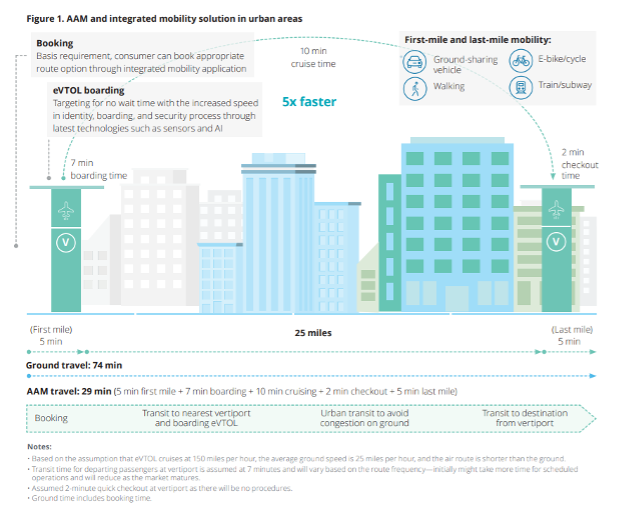

AAM promises to enhance the existing transportation ecosystem by addressing congestion and pollution.10 AAM offers the potential to increase the efficiency of current transportation networks by reducing travel time, improving sustainability, and expanding access to goods and services. AAM will be closely integrated with existing transportation networks and infrastructures for first- and last-mile connections.

It would be critical for operators to integrate AAM into the existing transportation system to create an integrated mobility solution in urban areas (figure 1). This new mobility solution can help determine the clear pathways for passengers, which could be essential to tracking routes and planning vehicle deployment.

Can AAM compete with the existing modes of urban transportation effectively?

AAM operators can compete with existing urban transport but must improve the economics to capture the market, as the demand will likely be directly proportional to the service price. A lower price per seat over time would likely create more demand, resulting in a high load factor because consumer willingness to pay for faster transportation is expected to be one of the primary factors driving AAM adoption. As the demand increases, higher production volumes could lead to economies of scale.

AAM economics depend to a large extent on the type of fleet, seating capacity, load factor, and length of flight routes. AAM operators should also establish a business model for pilot-operated eVTOL as the scaled commercial launch of autonomous eVTOL operations will at least be 10 years beyond the commercial launch of piloted eVTOL operations.11

Besides economics, safety, trip duration, and carbon footprint also play significant roles in driving the AAM market. In 2019, 37.5% of US CO2e from fossil-fuel combustion was registered from transportation activities, and a major portion is attributed to passenger cars, at 40.5%.12 Manufacturers of eVTOL claim zero operating emissions,13 and this new mobility system could achieve net-zero by cutting carbon from the related modes of transport during flight operations.14

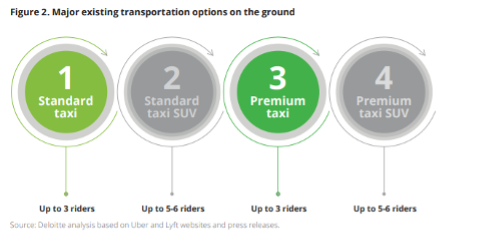

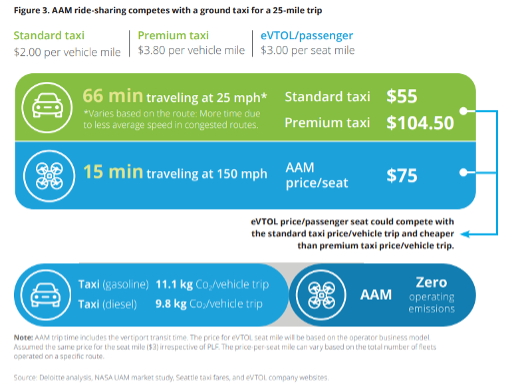

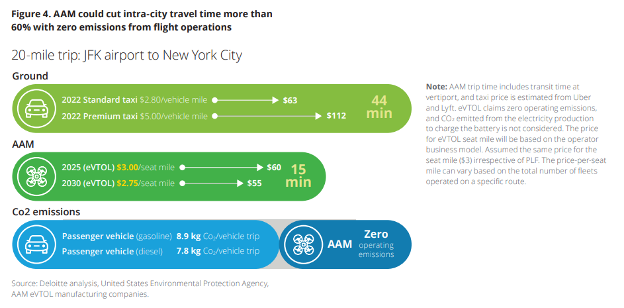

Standard taxi and ride-hailing services hold different fee structures—ride-hailing companies are priced less for passengers compared to traditional standard taxis. Hence, we have analyzed and compared AAM transportation with ground ride-hailing companies and taxis (figure 2). The standard taxi price in the United States largely varies between $1 and $3 to average about $2 per vehicle mile, and the premium taxi price ranges from $2.50 to $5 to average about $3.80 per vehicle mile.15 The AAM transportation mode could present an alternative to the premium taxi market for some trips due to passengers’ willingness to pay for the time and that it can be positioned as a luxury mode of transport. However, compared with the price-per-taxi vehicle miles, AAM ride-sharing is capable of competing with both standard and premium taxis as the anticipated price is almost equal. AAM seat mile price is estimated to be around $316 for a 4-seater eVTOL aircraft (figure 3).17 Ground transportation costs equate to more miles since the air distance between origin and destination (O&D) is shorter than on the road. On average, ground distance will likely be about 10% more than the air for a typical trip in a US city.18

The AAM industry is expected to mature rapidly toward high route frequency to provide quick and economical air travel for short distances. Unlike commercial aviation, limited seats in the eVTOL means operators’ need to achieve a 100% passenger load factor (PLF) will likely be crucial for staying competitive.

Also, the average cost per passenger could decrease as PLFs increase, driving eVTOL operators to provide AAM service at more competitive pricing. Deloitte’s analysis suggests that gasoline passenger vehicles emit about 404 grams of CO2 per mile19 and diesel passenger vehicles emit about 356 grams of CO2 per passenger mile. The eVTOL aircraft deliver greener trip options with zero operating emissions and could help in reducing carbon levels from the related modes of transport for the respective trip. The AAM transportation is capable of performing significantly better on time and carbon footprint, and could eventually compete with price by accessing the mass market.

AAM as a ride-hailing and ride-sharing service

Transporting people between and within cities, either scheduled or on-demand, could become a crucial application for AAM, where the most significant market is likely to exist. This is primarily because the AAM’s ultimate objective is to become a transportation system for mass transit, operating between urban, suburban, and rural areas. Among these two applications, intra-city transportation (transporting people and goods within cities) offers more value and is projected to fuel long-term growth. This is because they are shorter trips and address the burning issue of congestion. AAM ride-sharing services could drive the market for intra-city movement as the turnaround time could be as little as six to seven minutes20 for a 25-mile trip, and this time would be enough to charge the electric aircraft for the next trip. There is also expected to be the potential to reduce the price per passenger seat by about 8% in five years from inception with increased demand, larger fleet size, higher aircraft utilization, and PLF.

For instance, a passenger may be able to travel three times faster at the same price in a short 20-mile trip and assist in reducing about 8 to 9 kilograms of CO2, for example, from JFK airport to downtown New York City (figure 4).

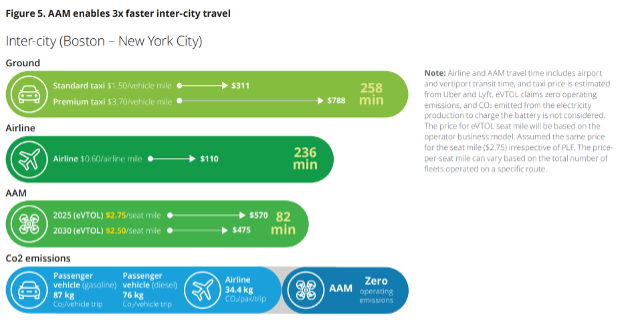

Due to reduced operating costs, the price-per-seat mile should be less for longer routes (inter-city). The passenger seat mile price is estimated to be $2.75 and could further decline to $2.50 by 2030 if the route matures with more demand, fleet, aircraft utilization, and PLF (figure 5). Usually, business travelers drive inter-city transport markets for quicker trips.

For instance, for a 190-mile trip between Boston and New York City, the passenger may be able to travel up to three times faster and cut about 80 kilograms of CO2. The aircraft turnaround time could be higher as the demand might not be high to fly back, and it could take about 60 minutes to charge the vehicle. A standard taxi for this route costs $1.50 per vehicle mile, and a premium taxi costs $3.70 per vehicle mile for the passenger to cover 215 miles in 258 minutes. An airline ticket is priced at about $110. While it is competitive with other ground options, it’s not viable given the time-consuming tasks at the airport. To/from airport journey time, airport departure/arrival process, and airtime make the total travel time almost equal to a ground taxi. Though airtime is virtually identical, associated functions at the airport make journey time longer than AAM. The AAM industry should aim to process passengers in less than five minutes since more time at the vertiport could hamper the potential of AAM as an alternative mode of transport—particularly for short/medium trips. The time variance should be significantly less between each connectivity mode to deliver faster travel. However, it would take a few years to provide a seamless travel experience for a passenger.

ICAO - Carbon Calculator, AAM eVTOL manufacturing companies

What should AAM companies do to drive faster adoption?

Cities’ growing need for new mobility options due to congestion, environmental challenges, and expanding access to communities, goods, and services could accelerate eVTOL aircraft use. However, unlike other rapid technological advancements—such as the swift adoption of smartphones—the advances in eVTOL use could gradually progress toward scale and mass adoption. AAM companies should choose the right aircraft, route, and business model to facilitate faster adoption based on the anticipated demand in different markets and regions.

Due to less turnaround time, short to medium-length routes could likely have higher traction for eVTOL operations in the initial stages. The development of integrated mobility applications that help consumers review all trip options, including first and last mile, could play a crucial role in the faster adoption of eVTOL aircraft. The existing sophisticated ground network could tie into an air mobility system to create a new transportation network, and consumers can access this network through an integrated mobility application. Such applications would provide the information to help customers compare and select the appropriate mode of transport or a combination based on the requirements. Furthermore, comparison across price, time, accessibility, and sustainability in the integrated mobility application could be critical in empowering people to make decisions.

The shared information between different parts of the transportation ecosystem will likely help determine the clear pathways for consumers and could be essential to track passengers or cargo and plan the vehicle deployment for the upcoming transportation leg.

Though every business model that AAM companies adopt should have a mix of aircraft configurations, higher aircraft utilization can be achieved by selecting appropriate aircraft configurations—more 4-to-6-seater aircraft mix for intra-city and lesser seat configuration for inter-city trips. To differentiate trips, operators should also ensure seamless, integrated transport options and less transit time between each mode to drive positive consumer perception around time and distance. Furthermore, AAM companies should identify routes where eVTOL operations can significantly impact time-saving during the initial launch phase.

Finally, optimal placement of ground infrastructure considering prime locations such as dense locations, business areas, airports, and areas with poor access or limited transportation options will likely be critical in driving demand for eVTOL operations. This means AAM companies should identify and focus on strategic locations for placing takeoff and landing infrastructure, such as vertiports.

Endnotes

1. Vertical Aerospace, The future of advanced air mobility, October 2021.

2. Vertical Flight Society, “Vertical Flight Society electric VTOL directory hits 600 concepts,” press release, January 21, 2022.

3. Joby Aviation, “Joby Aviation to list on NYSE through merger with Reinvent Technology Partners,” press release, February 24, 2021.

4. Archer Aviation, “Archer Aviation announces closing of business combination with Atlas Crest Investment Corp. to become a publicly traded company,” press release, September 16, 2021.

5. Lilium, “Lilium closes business combination with Qell Acquisition Corp., will begin trading on Nasdaq under symbol ‘LILM’ on September 15,” press release, September 14, 2021.

6. Vertical Aerospace, “Vertical Aerospace lists on NYSE following merger with Broadstone Acquisition Corp.,” press release, December 16, 2021.

7. Joby Aviation, “Joby nears completion of Part 135 Air Carrier Certification,” press release, March 15, 2022; Archer Aviation, “Archer takes to the skies with first hover flight of Maker craft,” press release, December 20, 2021; Lilium, “2021 Lilium year in review,” December 17, 2021; Volocopter, “Volocopter conducts first crewed eVTOL flight in France,” press release, March 24, 2022; eVTOL, “Hyundai’s Supernal explores eVTOL operations in Miami,” March 1, 2022.

8. John Coykendall, Aijaz Hussain, and Siddhant Mehra, “Operationalizing advanced air mobility: Preparing for long-term success,” Deloitte, 2021.

9. Vertical Flight Society, “Vertical Flight Society electric VTOL directory hits 600 concepts,” press release, January 21, 2022

10. Aijaz Hussain and David Silver, “Can the United States afford to lose the race?,” Deloitte Insights, January 26, 2021.

11. NASA, Urban air mobility (UAM) market study, November 2018.

12. US Environmental Protection Agency (EPA), Inventory of US greenhouse gas emissions and sinks: 1990–2019, 2021.

13. Joby Aviation, Corporate deck, March 29, 2022.

14. eVTOL aircraft have the potential to deliver net-zero emissions during flight operations depending on the power sources used to charge the aircraft.

15. Deloitte’s analysis based on publicly available data from leading ride-hailing companies in the United States.

16. Joby Aviation, Analyst Day presentation, June 3, 2021.

17. Joby Aviation, “Joby Aviation to list on NYSE through merger with Reinvent Technology Partners.”

18. Marco A. Diaz, Gregory W. Hendey, and Richard C. Winters, “How far is that by air? The derivation of an air:ground coefficient,” Journal of Emergency Medicine 24, no. 2 (2023): pp. 199–202. doi: 10.1016/s0736-4679(02)00725-4.

19. US Environmental Protection Agency, “Greenhouse gas emissions from a typical passenger vehicle,” accessed March 2022.

20. Sissi Cao, “A historic year for flying cars: 6 eVTOL companies dominating 2021,” Observer, December 27, 2021.

Authors

John Coykendall

Principal Global and US Aerospace and Defense leader

Deloitte Consulting LLP

+1 203 905 2612

Matt Metcalfe

Managing Director Government & Public Services

Deloitte Consulting LLP

+1 703 213 8029

Aijaz Hussain

Senior Manager US Industrial Products and Construction

Deloitte Services LP

+1 469 395 3759

Tarun Dronamraju

Assistant Manager

Deloitte Support Services India Pvt. Ltd.

+1 678 299 5358

Deloitte Research Center for Energy & Industrials

Kate Hardin

Executive director

Deloitte Research Center for Energy & Industrials

+1 617 437 3332

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Copyright © 2022 Deloitte Development LLC. All rights reserved