Production Increases Raise Fears Of Aircraft Order Bubble

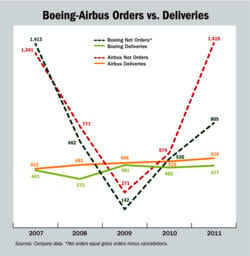

It is a truism of statistics that two people can study the same data and see radically different outcomes. Such is the case with the large commercial jet market. First, the facts: Airbus and Boeing took more than 2,200 net orders in 2011, twice the level of 2010 and far above the 1,011 jets they...

Subscription Required

This content requires a subscription to one of the Aviation Week Intelligence Network (AWIN) bundles.

Schedule a demo today to find out how you can access this content and similar content related to your area of the global aviation industry.

Already an AWIN subscriber? Login

Did you know? Aviation Week has won top honors multiple times in the Jesse H. Neal National Business Journalism Awards, the business-to-business media equivalent of the Pulitzer Prizes.

Related Content