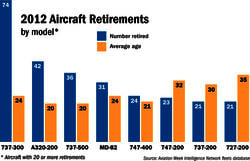

Perfect Storm Drives Part-Out Trend

In many ways, the aviation industry's business environment during the past few years has created a perfect storm for early aircraft retirements, reduced valuations and engine part-outs. Fuel prices are high, and new aircraft are on the way that promise savings of 15% or more on fuel costs. The...

Subscription Required

This content requires a subscription to one of the Aviation Week Intelligence Network (AWIN) bundles.

Schedule a demo today to find out how you can access this content and similar content related to your area of the global aviation industry.

Already an AWIN subscriber? Login

Did you know? Aviation Week has won top honors multiple times in the Jesse H. Neal National Business Journalism Awards, the business-to-business media equivalent of the Pulitzer Prizes.

Related Content