MRO Industry Girds For Aircraft Retirement Tsunami

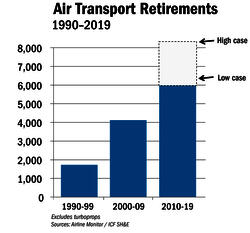

Today's news is peppered with accounts of the early retirement of passenger jets. In 2012 alone, 50 aircraft aged 15 years or less were retired from fleets. While such statistics make for good headlines, in reality those 50 accounted for less than 10% of the aircraft retired last year. It is the...

Subscription Required

This content requires a subscription to one of the Aviation Week Intelligence Network (AWIN) bundles.

Schedule a demo today to find out how you can access this content and similar content related to your area of the global aviation industry.

Already an AWIN subscriber? Login

Did you know? Aviation Week has won top honors multiple times in the Jesse H. Neal National Business Journalism Awards, the business-to-business media equivalent of the Pulitzer Prizes.

Related Content