Opinion: Bizjet Growth Eclipsing Stagnant Military Market

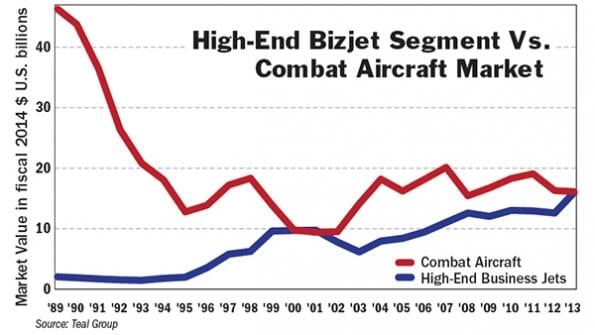

A version of this article appears in the May 5 edition of Aviation Week & Space Technology. H igh-end business jets are a strong market. General Dynamics’ first-quarter results, announced last month, show the continued evolution of the company from an almost pure-play defense prime to a company...

Subscription Required

This content requires a subscription to one of the Aviation Week Intelligence Network (AWIN) bundles.

Schedule a demo today to find out how you can access this content and similar content related to your area of the global aviation industry.

Already an AWIN subscriber? Login

Did you know? Aviation Week has won top honors multiple times in the Jesse H. Neal National Business Journalism Awards, the business-to-business media equivalent of the Pulitzer Prizes.