EU And Asean Aspire To An Open-Skies Treaty

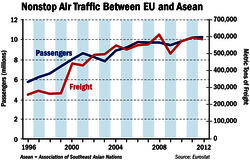

Legacy airlines in Europe and Asia have long recognized the Persian Gulf carriers as a major threat. Now the European Union and the Association of Southeast Asian Nations (Asean) are exploring an open-skies agreement that they hope will help defend their position and stop leakage of traffic to the...

Subscription Required

This content requires a subscription to one of the Aviation Week Intelligence Network (AWIN) bundles.

Schedule a demo today to find out how you can access this content and similar content related to your area of the global aviation industry.

Already an AWIN subscriber? Login

Did you know? Aviation Week has won top honors multiple times in the Jesse H. Neal National Business Journalism Awards, the business-to-business media equivalent of the Pulitzer Prizes.

Related Content